Active and Passive Vices…err…Voices…err…Values!

Ganga Prasad G. Rao

http://myprofile.cos.com/gangar

It was a dark storm that had engulfed the FinMin. The economy was in doldrums. Inflation was rampant, and every index of production intent on taking an ‘U’ and diving south. And to complicate matters, the capital markets were all too foresighted and taking plunges after plunges anticipating the economic downturn. The Economic Advisors to the Minister had their ear-ful but had nothing to offer beyond the usual prescriptions. With elections impending, the Minister was at his wits end, receptive to any suggestion, no matter how untried and untested to shore up his party at the polls. Now there’s always one who awaits the ‘Opportunity knocks but once’ circumstance. And who could it be but the infamous Iamsly. Years,… no, decades of doing business with corrupt politicians, whom he had enriched with crumbs from the mineral resources he had exploited, had turned him a billionaire many times over. Call it the pangs of patriotism, empathy for the profession/industry, or a desire to ‘give back’ to those whom he had so mercilessly exploited, but Iamsly was willing to consider a ‘not insubstantial’ donation to a few ‘worthy’ causes, if his excesses were overlooked. Christmas is all about giving, isn’t it?

Does it take a soothsayer to predict what happens when desire meets urge? Or, when one hears a rumor of money to be given away? They turned up sooner than a fly seeks spilled syrup! …Predictably, the first one thru the door claimed to represent those impenured by Iamsly’s International mining firm, in fact representing those accursed in the ‘resource curse’ era. Rubbing shoulders, the other smiling face offered his credentials; he represented the environmentally exploited, and yet in poverty. And forcing her way between the two, the fat lady drew Iamsly’s attention with her charm as she introduced herself as the Head of the Charities for the Aborted Unborns (and,sly sly, MIAs). Behind her was a, … well, many with their begging bowls, small, large, and… hmm.

Was it strategic, genius, or a mere coincidence when Iamsly’s Advisor-Son-Heir apparent -let’s call him Ash shall we? - suggested a ‘tri-partite’ round of Golf meeting between Iamsly, the Minister and the representatives of the various Charities? Perhaps the ‘unscheduled’ mid-term elections were around the corner, for the Minister, uncharacteristically, willingly accommodated the golf picnic, albeit after insisting upon an Attorney by his side. And so, they congregated, in the shade of the White Oak by the golf course. The preliminaries behind, Ash put forth his proposal. He recalled that, over the decades, the nation had witnessed several regime changes – from democratic to dynastic, autocratic to dictatorial…and that Iamsly was an ardent supporter of consensual democracy. Ash pressed the point that tax laws were obeyed more in the exception in those ‘doldrum’ years, then fixed against the Resource barons - ostensibly so the nation could tide over its growing pains, then overturned again to accommodate a dictator’s vengeance, and now were being repealed all over again. Was it Iamsly’s fault that he was incriminated in a dozen tax claims across three decades?

The pressure of the upcoming unscheduled mid-terms must have been intense, for the Minister was all ears. He wondered what the heir had in mind to resolve the matter?Capitalizing on the opportunity, Ash was quick to his point:Shouldn’t the Government, in the spirit of ‘reconciliation’, forgive prior the elections, the (tax) excesses of years past? Referring obliquely to the 2 dozen tax cases that he would inherit, Ash, proposed that the Ministry could repeal the tax laws and permit negotiated tri-partite settlements that channelled the disputed tax amounts to ‘worthy’ causes. Couldn’t we, argued Ash persuasively, in the spirit of the Yuletide, ….ahem…. add a clause that permitted Charities and NGOs to bid for the disputed tax monies set aside in escrow accounts? Why, they could compete amongst themselves in bidding rounds by varying the ‘degree of forgivance’ they would offer to the defendant, to sway the donation their way, and thus resolve the dispute amicably. What Ash didn’t divulge was his hope that the more severe the crash crunch the NGOs and charities faced, the worthier and the less-correlated their cause, (or, the looser their principles) the larger would be the degree of tax forgivance they would risk in the bidding rounds. Plainspeak: Forgive my ‘the-axe’ excesses and I fill your stockings!.

The Attorney interrupted Ash as he outlined his proposal, and insisted that any tax settlement be recorded formally as an affidavit in the arbitration documents to be signed by the Minister. But it was the Minister who foresaw that Iamsly(and his ilk) would get away with looting the Fort Knox in broad daylight, what with several Charities bidding for the ‘escrow largesse’. Uprightly, he insisted that the ‘forgivers’ have choice aplenty as to the party with whom to engage in the ‘forgivance business’. Surprised with the Minister’s acumen, Ash presumed the Minister would also be wise to the possibility NGOs would cross-compete and forgive the grossest of sins, crimes and evasions in bidding against each other even as they defended their own turf in interests dear to them. And indeed, the Minister, fearing the subversion of Justice, sought the opinion of the bemused Attorney, who suggested a EqSF/EfSF variant, that empowered those NGOs that truly believed in their cause, to outbid the more forgiving and the less-principled amongst them, and claim restitution for the ‘unforgiven’ wrongs via the ‘Bond market – Full key’ resolution. Ash cringed at the prospect of the bond market playing volatility on his escrow until the wrong was corrected, but played along fearing the talks would break down.

In the months that followed Iamsly, Ash, and those other Iamnasty,gathered under the watchful eye of the Attorney as the various charities and NGOs – environmental, health, social, animal rights, gay rights, you name it – bid against each other to offer various degrees of ‘tax forgivances’. A case of a $10 million tax avoidance was bid up to 60% forgivance, in return for a $2 million endowment to the environmental organization.A ‘tax case’ involving oil spill in the Mid-Atlantic counted for near nothing in a settlement with a Gay rights organization – the guilty excused a good 90% of his oil spill dues. In another dispute, a firm in the dock for a Superfund NIMBY violation, was cornered with a ‘meet you half-way’ offer by the Vietnam Vets,literally for the cake!Worse, a case of ‘Leaded Gasoline with 6% Benzene’ was bid away by an EqSF environmental organization that sponsored and underwrote a new issue of ‘Education for the Poor’ bonds with the wrong.

A lonely intern whom the Attorney had accompany him, took note of the ‘principals’ and ‘principles’ involved in the ‘tax forgivance – sin encashing – fund raising’ trading sessions, in particular the implicit ‘premiums and discounts’ across the various settlements. He hoped to collect sufficient data to put together a model that would facilitate the elicitation of overt and passive values for environmental and social causes, as well as WTAs among the ‘Forgivers’,and WTPs among the ‘Forgiven’ for various environmental sins that fouled the commons. He hypothesized that an incentive existed to permit the proliferation of Charities and NGOs, staff them with unethical managers, and hold their finances on a leash, so they’d be willing, even waiting to ‘forgive and forget’ the sins, omissions and commissions of the industry for a pittance. He hoped to get a Master’s thesis out of it. As for his thesis committee, the Attorney was already weighing upon him.....and an Iamnasty waiting in the wings to fund him even an entire year.

Here’s wishing him all luck! (and, years to his life)

Au Revoir !

Wednesday, December 28, 2011

Sunday, December 18, 2011

Transition Robonomics!

Transition Robonomics !

Ganga Prasad Rao

http://myprofile.cos.com/gangar

Economics might be the Les Miserables of Social Sciences, but that did not stop John Jetson from day dreaming between his shifts as a week-on/week-off temp at the automobile factory and the Masters he pursued at the local Community college. And day dream he did, between his gulps of beer while fixing a tyre on his Chevy….this being a warm Sunday afternoon in August ….of a world in which he would wake up to breakfast served in bed by his very personal robot, of being robot-driven thrice a week to his very own Executive office, and apprised of his appointments by a robot Secretary, then supervising robots assembling robots, ….and, not to forget, lazing in the sun between work days writing lyrics set to robot music. But an all too familiar shrill voice woke him up. With a cantankerous 2-year old on one arm and a suckling baby on the other, his wife of 4 years was berating him to find a ‘real’ job, a full-time job that would bring soup to the dinner table instead of a ‘back to school’ program in Economics at 42 that impoverished the growing family.

“God”, Jetson murmured to himself, “should have turned certain female frequencies inaudible to men”. Honestly, why would anyone want to work when robots were at his beck and call? But reality got the better of his virtual self. Only last month had the smart-alec Engineers put the finishing touches on an AI-enhanced robot assembly line at the automobile factory south of Main Street. The entire community was outraged at the carnage that followed; the labor force cut in half and their families on the road on the double. And yet, it was necessary for the Big 4th to retain its share in the auto market and survive to fight another day. Besides, there weren’t too many employers waiting to offer him wages that supported his family and the College. Caught between a rock and a hard place, Jetson Sr. wondered why labor-saving technological change, a concept he had been taught in Production Economics, should bring misery to those who could least afford it? And what could the Government do to anticipate a world of robots running our factories? Couldn’t anyone find a “…..Hey, that could be my Master’s paper, even my ticket to graduation!” With a twinkle in his eye….and a mollifying hug and kiss…Jetson Sr., set out in his run-down Chevy to the College library with a scratch pad to prove his genius and, just perhaps, start along a new road, to new career.

Thank the Good Lord for mercies small and ...hmm?,... for the library was open, perhaps anticipating sophomores returning to school for an early start on their Fall semester. Jetson found a corner table, and literally ‘hit the books’. Taught to be methodical in research, Jetson began by writing down his objective: to maximize an Aggregate Social Welfare Function, SWF, for the society in general, but in particular labor, subject to various constraints that included the nation’s macroeconomic identity, an industry aggregate profit function, a population-evolution function, a ‘labor-supply’ function, a ‘Social’ (as opposed to ‘Private’) Resource discovery-cum-Reserve transformation function, and ancillary functions governing capital, wage and price formation in the economy. The objective and the constraints identified, Jetson began by specifying the Resource-Reserve functions. There was the conundrum of specifying the process of Resource discovery, and the transformation of Resources to Reserves. He addressed it by positing a 2+1 set of functions and identities.

The first function, ResDisc, represented the process of resource discovery as a multiplicative probabilistic process: the success rate being both a function of cumulative resources discovered and the Exploration Budget, ExpBud in the current period. The latter was a function of many variables, including Lifestyle expectations, LS, discount rate, r, rental rate of Capital, v, per-capita consumption, C/Pop (= y), ratio of domestic to international (resource) prices, p/P, Population, Pop, and Economic Policies, EcPol. The identity represented the addition of discoveries to the Resource Base, RoB. To model Reserve Base, ReB, the currently economic portion of the resource base, Jetson specified a third function of domestic and international prices, p & P, technology embedded in (net) capital investment, IT, capital K, wages, w, and a variable denoting the comprehensiveness and stringency of Environmental Regulations, ESHReg.

Next, he turned his attention to a Population growth function. Given the lags and the inertia of population dynamics, he chose the widely used Koyck-lag specification around an optimal Population, Pop*:

In his model, Population responded to changes in the underlying determinants and moved toward the target, Pop*, across time periods. The target, ‘optimal’ population was influenced by Lifestyle expectations, LS, the aerial extent of the political entity, D, National wealth, W, Capital, K, per-capita income, y (=Y/Pop), the price level, p, and notably, a measure of the economic policies followed by the political entity, EcPol (an euphemism for the extent of subsidy in the economy and trade policy). The National Wealth variable, W, was the aggregate value of net monetary (Liquid assets + Equity - Debt), ‘Real’ Land Assets, Gold, and further, included the imputed net present value of natural (in particular, mineral)-resources, ReB, that passed the definition of a ‘Reserve’.

Moving next to Labor Supply, Jetson modelled the fraction of population, Lf, seeking employment at any time, t. It had as its arguments, per-capita income, y, lifestyle expectations, LS, prices, p, wages, w and Wealth, W:

Thankfully, the National Macro-economic identity was easily specified:

where Y denoted GDP, C stood for Consumption, G for Government Spending (Infrastructure, ESH and Equity), and XM represented a net trade function.

For modelling factor demands, Jetson Sr. chose an Aggregate Industry Profit function, hoping the choice would enable lateral use in macro-financial modelling. pirepresented the sum of Retained Earnings, RE, and Dividends, Div. There was an additional complication concerning the nature of technical change – whether embodied, or disembodied. Jetson preferred the simpler alternative of technology manifesting itself via capital replacement. Embedded within the Profit function was a KLEM production function enhanced with Net Technical change, IT, and EnvReg as critical endogenous variables:

Jetson realized that for a large macro-system, the evolution of prices, p, a crucial determinant of lifestyle, too was of interest. He therefore posited a price-evolution function:

in which prices moved with per-capita consumption, capital, wages, GDP growth rate, international prices, economic policy and environmental regulation.

Finally, he turned his attention to the specification of the ‘Wage Evolution’ function. Well aware of the dichotomy between macro- and micro-economics as regards the endogeneity of wages, Jetson chose to model it endogenously given his intended focus on macro-labor policy. In specifying the wage evolution function, the Sr. envisaged it to be influenced, beyond the ‘tightness’ of the labor market, by the labor-saving nature of technical change, IT, as well as capital in place, Kt-1, the ratio to domestic to international prices, and Economic Policy:

With the above definitions and specifications in place, Jetson specified the SWF, given its political sensitivity, with particular attention to the labor market. He figured the society would seek to maximize employment among those seeking jobs, Lw/Lf, per-capita income, y (= Y/Pop), wealth, W, and ESH standards, but hold down the cost of living as represented by the vector of real prices, p. Thus, motivated, the SWF function read:

Gingerly, Jetson penned the ‘grand optimization system’ to sustain Social Welfare in a dynamic, capitalist system characterized by cost-cutting, labor-saving technical change:

Solving the 12-equation model was a monstrosity given the lags and inter-dependencies, but Jetson had the benefit of an ‘equation-crunching’ optimizing software on the ‘Cloud-enabled’ library computers that aided the analytical derivation of the critical relationships. Beyond the maximized SWF (and optimal factor demands), the rules specified a) Economic policies necessary to obtain an optimum population time profile that fit the larger optimization of social welfare, b) the implied optimum rate of change of technology-embodying capital, and, c) the implied relationship between labor demand and wages consistent with a scenario of continued labor-saving technical change and population projections.

Jetson didn’t like what he saw in the outputs spit out by the optimization routine. Yes, capital accumulation and reserve addition drove output growth, but population was a damper on wages. Life-style expectation and Economic policies played an important role in the economic growth of the society. ESH Regulations impacted upon labor supply thru its impact on living standards.

The optimal short-run labor demand, L*, was of the general form:

The coefficients indicated that optimal labor use, expectedly, fell with wages and capital in place, and with the pace of introduction of labor-saving technical change. Free trade resulted in labor-saving imports in times when p > P in sectors with k/l < K/L. The implied Capital-Investment, IT* was a function of the wage-rental ratio, the ratio of domestic to international prices, Economic policy, and Lifestyle Expectations, among other factors. Labor-saving technical change, motivated by the necessity to reduce costs and increase profits, would necessarily imply either a steep reduction in labor use and/or a significant drop in real wages in manufacturing. Given the ‘momentum’ in population growth, the prevalence of per-capita, subsidy-pandering politics, the arrival of AI-enhanced robot and automation technology, and aware of the ‘sacred cow’ that employment was, Jetson foresaw a tendency to politically accommodate blue-collar labor far beyond what was cost-efficient for the technically-advanced economy. The maximization of the SWF implied the society either manipulate trade policy in labor-intensive sectors, hold back technical change, reduce labor use, or accept deep cuts in blue-collar wages to accommodate advanced, cost- and labor-saving technology. It is surprising how even otherwise ordinary people rise to the occasion in times of crises. A humble roughneck though, Jetson foresaw a distant cloud of social strife if capitalism were to be pursued to its logical end. For a society to reap the benefits of advanced technology – the outcome of an elaborate system of education and research supported annually with billions of dollars worldwide, and employing the best of global talent - it’d be necessary to resolve the issue of Manufacturing Labor-employment and wages. It would be a challenge to a society that had stressed technology without anticipating suitable policies to address its social impacts; in fact, and to the opposite, even exacerbating it in to a crisis with its per-capita-based subsidy policies. Jetson perceived an opportunity to design a policy resolution to address the same. And although he hadn’t modelled it, Jetson anticipated that in all likelihood, the rise in incomes among households in a high-efficiency, high profit world would imply a concomitant increase in demand for service-sector employees, as affluent households demanded personal attention and customized services. It was perfunctory then to first consider a flexible mechanism for facilitating the smooth transfer of Manufacturing Blue-collar labor to the Service industry. With a deep sense of responsibility to future generations, he scoped out the ‘2-pronged Jetson Proposal’: the first part being a rather simple ‘Labor Switch-Points’ module, and the second, a more involved ‘Macro-financial’ module. The intention behind the ‘Labor Switch-Point’ construct was to both inform potential blue-collar Manufacturing labor of their relative likelihood of continued employment given changes in the underlying ‘shadow wages’ upon the advent of labor-saving technical change, and simultaneously offer a formal, automated mechanism to bring about a smooth transition in to employment in the Service sector. Toward that objective, Jetson posited both a ‘Switch Point Demand’ function and a ‘Switch Point Supply’ function - akin to Excess Labor Supply & Demand functions:

Jetson modelled the Service Sector as demanding Switch points, SwPtDS; the demand increasing in Service sector Output, Ys, but decreasing in manufacturing wages, wM, and Experience, ExpM, of prospective Manufacturing employees. To factor in family-stage-specific circumstances that obstructed the transition, he included, Dep, representing the number of dependents, as an additional variable (Jetson gulped hard for what it meant in his case). In a similar vein, the Supply of Manufacturing Sector Switch points, SwPtSM increased in wages, wM, and Net Investment, IT, but decreased in own Output, YM. In addition, Jetson added a variable, FD, representing Cumulative FDs subscribed to by Blue collar labor in lieu of wages (Jetson made a mental note to explain later what he meant by his ‘Wage-FD’ strategy). It captured the employer’s proclivity to retain employees willing to sacrifice wages for long-term financial security.

The demand and supply functions specified, Jetson set the ball rolling. He required a pan-industry Labor Organization to minimize the area to the left and below the intersection of the two functions in the SwPt–wM space. The intersection of the SwPt Demand function with the SwPt Supply function (plotted against wM) revealed the optimal Switch Points, SwPt*, below which the Service Sector made ‘Wage-protected’ offers to ‘redundant’ manufacturing employees. The equilibrium SwPt* varied with both Supply and Demand factors, thus lending a touch of uncertainty and cyclicity to the process of Labor migration. The Switch Point strategy facilitated the smooth transfer of Manufacturing labor to the Service Sector while protecting wages, and offered blue-collar labor the opportunity to tune their wages and savings in line with economic and labor-market prospects.

Having designed a mechanism that provided for a smooth adjustment in the Labor market, Jetson chose strategically to aggregate the Blue-collar work force across all Manufacturing industries separate from Service Sector Employees (in which, he included the Manufacturing White Collar employees as well). Next, he bought in to the Blue Collar Pension Fund Authority, PFA, which managed FD contributions as well as the stock purchases and bond assignments to each employee’s portfolio). He intended, given his read of the future, that the Blue-collar PFA would facilitate the implementation of a policy that would, in essence, reduce the wage-rental ratio, w/v, in each sector to that consistent with a robot economy as revealed in the K*, IT*, and L* expressions. In essence, he achieved it by offering wealth compensations to induce voluntary reductions in wages. Each blue-collar employee, whether in Manufacturing or Service Sector, was offered as much in stocks and bonds as the reductions he or she accepted from wages, toward purchase of Long FDs in to his or her pension account. The FDs, and the bundled, matched Stocks/Bonds ensured employees were left at least as well-off in the immediate term, and likely wealthier in the long-run. In this manner, Jetson de-linked wages from work hours, and effectively reduced the wage-rental ratio as it applied to, or, was perceived for operational and investment decisions, thus facilitating a transition to an AI-Robot Economy. Employees too, factored in the wage reduction for their consumption decisions, but made longer term lifestyle decisions based on assets they held with the PFA.

In choosing their Stock compensation for wages ‘sacrificed’ to the future as FDs, Blue collar employees were permitted their choice of stocks between ‘Own firm stock’, a zero-correlation ‘Perpendicular firm stock’ and a broad Stock market Index fund. The Employer, however, deferred the issue of FDs funds; instead it guaranteed ‘Earned Wage Payables, EWP, issued by the PFA. EWPs represented a ‘wages payable’ against the Employer, and listed as an ‘asset’ on PFA books in the sense it was liquid and could be encashed on demand. These EWPs were taken a lien upon by the pan-industry Blue-collar Labor Union, after which the PFA issued FD credits, FDCs (a ‘legal-twist’ that Jetson leveraged for a larger resolution) to the pension accounts of its subscribers.

Yet weary from thinking thru the first part of his proposal, Jetson moved on to the second. Lest the ‘wealth compensation for wage sacrifice’ strategy be presumed a mere re-classification of compensation, and given potential impacts upon various facets of the society, Jetson hastened to unravel a larger resolution for the Robotmation economy. In his resolution, the Fed was an independent agency in charge of ensuring financial stability – a charge that included the management of currency, bank deposits, bullion, interest rates and foreign exchange. Now, the Fed, as part of its duty to ensure financial stability, managed Asset-Liability balance of the economy, with a ‘back of the envelope’ thumb rule:

In the context of his task, Jetson imagined a creative re-interpretation of the above:

The Fed accommodated the demand for currency arising from the growth in Net Assets by either permitting or issuing IPOs/FPOs, issuing FDs or Long Bonds, or by managing its Foreign Currency and Bullion operations. Jetson was no genius, but he found the EWPs (which constituted an ‘earned payable’, a ‘Receivable’ on PFA books, and upon which the FDCs were issued), both an excellent ‘raison d’etre’ and a suitable ‘collateral’ for the issue of new Currency during asset re-balancing operations. By his reckoning, the Fed, rebalanced assets and liabilities around its endogenous instruments – the issue/manipulation of Currency, Bullion, IPO/FPO, Foreign exchange and Long Bonds. Jetson first required that Bullion be adjusted to cancel out changes in the FD and Foreign currency holdings:

Thus cancelled out, the Asset-Liability balance reduced to:

By his 2-step resolution, the Fed on one hand, adjusted its bullion operations to cancel out against foreign exchange and FD(C)s issued, and on the other, issued new Currency to equal the sum of IPO/FPO and Long Bonds issued. The Fed paid for the use of EWPs by ‘sponsoring’ the conversion of FDCs to FDs that were in turn credited in to the accounts of the Blue-collareds at the PFA. The Government ‘bought’ the new issue of Long Bonds from the Fed (or, equivalently, sponsored them), and forwarded them to the PFA toward its match for the participation of employees in the ‘Robotmation scheme’. In addition, the Government strategically bought in to the IPO/FPO so it could recover tax revenues lost from ROE-based tax-credits that it offered to firms when the stock appreciated post the rise in profits following introduction of Robotmation. Compensated, on one hand, with ROE-based tax credits, and relieved of immediately making good on the EWPs, manufacturing firms offered larger discounts on their stocks to their blue-collared employees in their ESOPs to pave the way for robotmation. The discounts, funded by the deferred EWP and limited to FD subscribers, served to further incentivize the participation of the Blue-collared in the ‘Robot Economy’.

Tying the loose ends, Jetson confirmed that his 2-pronged proposal compensated the wage sacrifices made by the Blue-collared labor in anticipation of a Robot economy three ways – FDs, Employer-discounted stocks, and Government-sponsored Long Bonds. Jetson verified that the Blue-collar Union cancelled its lien on the EWPs, and the PFA recovered its FD ‘principal’ – the face value of the EWPs issued – when the Fed ‘sponsored’ the conversion of FDCs to FDs. The Employers leveraged, and made good their deferred FD obligations to the PFA, by funding a discounted Stock offer to participating employees. The Government, too, found it convenient to leverage the issue of Long bonds by the Fed toward its Bond-obligations to the Blue-collar PFA. Further, it found the IPOs/FPOs a convenient asset class to invest in and recover tax revenues lost when those stocks appreciated upon the realization of higher profits following introduction of ‘robotmation’.

The bell rang to alert users the Community College Library closed 6pm sharp. Jetson barely had a minute or two on hand. Hurriedly he scribbled that his 2-pronged solution was of a pareto-nature that benefited all stakeholders – Labor, Capitalists, the Government and the broader society. The three-way compensation to the labor, and the ‘pareto’ nature of adjustments and incentives offered to the Industry and the Government brought about a much faster transition to Robotmation than was considered feasible.

Robotmation was both an opportunity and a threat to humanity’s future. Compensated with wealth accretions, Jetson had eased the Blue-collareds in to an orderly inter-generational transfer to the Robot economy without the mass unemployment and the social strife that had bedevilled other proponents. His resolution, in fact, anticipated and reduced the threat of social discord, while preserving the opportunity of genuine economic gain that a Robot economy offered. His brand of Robonomics was, he felt, particularly appropriate to per-capita-based subsidy economies grappling with a population crisis and a large public sector– a description that fit many emerging nations. But more to his ideals, Jetson believed his proposal was an appropriate transition policy from an inefficient/per-capita, subsidy-based, socialist economy toward a high profit, distributed capital ownership-based, and more efficient Closed Cycle/Robot Economy. It’d interest policy makers and politicians alike for the manner in which it tackled a highly sensitive social issue. The Jetson brand of finance was particularly apt to....

Interrupting himself before he could be shooed away by the library staff, Jetson walked out in to the yet warm late afternoon Sun. As he got to the Chevy, the sun glinting off its windshield, he thought ‘Gotta get the steering fixed soon’.

….. And no day-dreaming on the snaky way back home either!

Ganga Prasad Rao

http://myprofile.cos.com/gangar

Economics might be the Les Miserables of Social Sciences, but that did not stop John Jetson from day dreaming between his shifts as a week-on/week-off temp at the automobile factory and the Masters he pursued at the local Community college. And day dream he did, between his gulps of beer while fixing a tyre on his Chevy….this being a warm Sunday afternoon in August ….of a world in which he would wake up to breakfast served in bed by his very personal robot, of being robot-driven thrice a week to his very own Executive office, and apprised of his appointments by a robot Secretary, then supervising robots assembling robots, ….and, not to forget, lazing in the sun between work days writing lyrics set to robot music. But an all too familiar shrill voice woke him up. With a cantankerous 2-year old on one arm and a suckling baby on the other, his wife of 4 years was berating him to find a ‘real’ job, a full-time job that would bring soup to the dinner table instead of a ‘back to school’ program in Economics at 42 that impoverished the growing family.

“God”, Jetson murmured to himself, “should have turned certain female frequencies inaudible to men”. Honestly, why would anyone want to work when robots were at his beck and call? But reality got the better of his virtual self. Only last month had the smart-alec Engineers put the finishing touches on an AI-enhanced robot assembly line at the automobile factory south of Main Street. The entire community was outraged at the carnage that followed; the labor force cut in half and their families on the road on the double. And yet, it was necessary for the Big 4th to retain its share in the auto market and survive to fight another day. Besides, there weren’t too many employers waiting to offer him wages that supported his family and the College. Caught between a rock and a hard place, Jetson Sr. wondered why labor-saving technological change, a concept he had been taught in Production Economics, should bring misery to those who could least afford it? And what could the Government do to anticipate a world of robots running our factories? Couldn’t anyone find a “…..Hey, that could be my Master’s paper, even my ticket to graduation!” With a twinkle in his eye….and a mollifying hug and kiss…Jetson Sr., set out in his run-down Chevy to the College library with a scratch pad to prove his genius and, just perhaps, start along a new road, to new career.

Thank the Good Lord for mercies small and ...hmm?,... for the library was open, perhaps anticipating sophomores returning to school for an early start on their Fall semester. Jetson found a corner table, and literally ‘hit the books’. Taught to be methodical in research, Jetson began by writing down his objective: to maximize an Aggregate Social Welfare Function, SWF, for the society in general, but in particular labor, subject to various constraints that included the nation’s macroeconomic identity, an industry aggregate profit function, a population-evolution function, a ‘labor-supply’ function, a ‘Social’ (as opposed to ‘Private’) Resource discovery-cum-Reserve transformation function, and ancillary functions governing capital, wage and price formation in the economy. The objective and the constraints identified, Jetson began by specifying the Resource-Reserve functions. There was the conundrum of specifying the process of Resource discovery, and the transformation of Resources to Reserves. He addressed it by positing a 2+1 set of functions and identities.

The first function, ResDisc, represented the process of resource discovery as a multiplicative probabilistic process: the success rate being both a function of cumulative resources discovered and the Exploration Budget, ExpBud in the current period. The latter was a function of many variables, including Lifestyle expectations, LS, discount rate, r, rental rate of Capital, v, per-capita consumption, C/Pop (= y), ratio of domestic to international (resource) prices, p/P, Population, Pop, and Economic Policies, EcPol. The identity represented the addition of discoveries to the Resource Base, RoB. To model Reserve Base, ReB, the currently economic portion of the resource base, Jetson specified a third function of domestic and international prices, p & P, technology embedded in (net) capital investment, IT, capital K, wages, w, and a variable denoting the comprehensiveness and stringency of Environmental Regulations, ESHReg.

Next, he turned his attention to a Population growth function. Given the lags and the inertia of population dynamics, he chose the widely used Koyck-lag specification around an optimal Population, Pop*:

In his model, Population responded to changes in the underlying determinants and moved toward the target, Pop*, across time periods. The target, ‘optimal’ population was influenced by Lifestyle expectations, LS, the aerial extent of the political entity, D, National wealth, W, Capital, K, per-capita income, y (=Y/Pop), the price level, p, and notably, a measure of the economic policies followed by the political entity, EcPol (an euphemism for the extent of subsidy in the economy and trade policy). The National Wealth variable, W, was the aggregate value of net monetary (Liquid assets + Equity - Debt), ‘Real’ Land Assets, Gold, and further, included the imputed net present value of natural (in particular, mineral)-resources, ReB, that passed the definition of a ‘Reserve’.

Moving next to Labor Supply, Jetson modelled the fraction of population, Lf, seeking employment at any time, t. It had as its arguments, per-capita income, y, lifestyle expectations, LS, prices, p, wages, w and Wealth, W:

Thankfully, the National Macro-economic identity was easily specified:

where Y denoted GDP, C stood for Consumption, G for Government Spending (Infrastructure, ESH and Equity), and XM represented a net trade function.

For modelling factor demands, Jetson Sr. chose an Aggregate Industry Profit function, hoping the choice would enable lateral use in macro-financial modelling. pirepresented the sum of Retained Earnings, RE, and Dividends, Div. There was an additional complication concerning the nature of technical change – whether embodied, or disembodied. Jetson preferred the simpler alternative of technology manifesting itself via capital replacement. Embedded within the Profit function was a KLEM production function enhanced with Net Technical change, IT, and EnvReg as critical endogenous variables:

Jetson realized that for a large macro-system, the evolution of prices, p, a crucial determinant of lifestyle, too was of interest. He therefore posited a price-evolution function:

in which prices moved with per-capita consumption, capital, wages, GDP growth rate, international prices, economic policy and environmental regulation.

Finally, he turned his attention to the specification of the ‘Wage Evolution’ function. Well aware of the dichotomy between macro- and micro-economics as regards the endogeneity of wages, Jetson chose to model it endogenously given his intended focus on macro-labor policy. In specifying the wage evolution function, the Sr. envisaged it to be influenced, beyond the ‘tightness’ of the labor market, by the labor-saving nature of technical change, IT, as well as capital in place, Kt-1, the ratio to domestic to international prices, and Economic Policy:

With the above definitions and specifications in place, Jetson specified the SWF, given its political sensitivity, with particular attention to the labor market. He figured the society would seek to maximize employment among those seeking jobs, Lw/Lf, per-capita income, y (= Y/Pop), wealth, W, and ESH standards, but hold down the cost of living as represented by the vector of real prices, p. Thus, motivated, the SWF function read:

Gingerly, Jetson penned the ‘grand optimization system’ to sustain Social Welfare in a dynamic, capitalist system characterized by cost-cutting, labor-saving technical change:

Solving the 12-equation model was a monstrosity given the lags and inter-dependencies, but Jetson had the benefit of an ‘equation-crunching’ optimizing software on the ‘Cloud-enabled’ library computers that aided the analytical derivation of the critical relationships. Beyond the maximized SWF (and optimal factor demands), the rules specified a) Economic policies necessary to obtain an optimum population time profile that fit the larger optimization of social welfare, b) the implied optimum rate of change of technology-embodying capital, and, c) the implied relationship between labor demand and wages consistent with a scenario of continued labor-saving technical change and population projections.

Jetson didn’t like what he saw in the outputs spit out by the optimization routine. Yes, capital accumulation and reserve addition drove output growth, but population was a damper on wages. Life-style expectation and Economic policies played an important role in the economic growth of the society. ESH Regulations impacted upon labor supply thru its impact on living standards.

The optimal short-run labor demand, L*, was of the general form:

The coefficients indicated that optimal labor use, expectedly, fell with wages and capital in place, and with the pace of introduction of labor-saving technical change. Free trade resulted in labor-saving imports in times when p > P in sectors with k/l < K/L. The implied Capital-Investment, IT* was a function of the wage-rental ratio, the ratio of domestic to international prices, Economic policy, and Lifestyle Expectations, among other factors. Labor-saving technical change, motivated by the necessity to reduce costs and increase profits, would necessarily imply either a steep reduction in labor use and/or a significant drop in real wages in manufacturing. Given the ‘momentum’ in population growth, the prevalence of per-capita, subsidy-pandering politics, the arrival of AI-enhanced robot and automation technology, and aware of the ‘sacred cow’ that employment was, Jetson foresaw a tendency to politically accommodate blue-collar labor far beyond what was cost-efficient for the technically-advanced economy. The maximization of the SWF implied the society either manipulate trade policy in labor-intensive sectors, hold back technical change, reduce labor use, or accept deep cuts in blue-collar wages to accommodate advanced, cost- and labor-saving technology. It is surprising how even otherwise ordinary people rise to the occasion in times of crises. A humble roughneck though, Jetson foresaw a distant cloud of social strife if capitalism were to be pursued to its logical end. For a society to reap the benefits of advanced technology – the outcome of an elaborate system of education and research supported annually with billions of dollars worldwide, and employing the best of global talent - it’d be necessary to resolve the issue of Manufacturing Labor-employment and wages. It would be a challenge to a society that had stressed technology without anticipating suitable policies to address its social impacts; in fact, and to the opposite, even exacerbating it in to a crisis with its per-capita-based subsidy policies. Jetson perceived an opportunity to design a policy resolution to address the same. And although he hadn’t modelled it, Jetson anticipated that in all likelihood, the rise in incomes among households in a high-efficiency, high profit world would imply a concomitant increase in demand for service-sector employees, as affluent households demanded personal attention and customized services. It was perfunctory then to first consider a flexible mechanism for facilitating the smooth transfer of Manufacturing Blue-collar labor to the Service industry. With a deep sense of responsibility to future generations, he scoped out the ‘2-pronged Jetson Proposal’: the first part being a rather simple ‘Labor Switch-Points’ module, and the second, a more involved ‘Macro-financial’ module. The intention behind the ‘Labor Switch-Point’ construct was to both inform potential blue-collar Manufacturing labor of their relative likelihood of continued employment given changes in the underlying ‘shadow wages’ upon the advent of labor-saving technical change, and simultaneously offer a formal, automated mechanism to bring about a smooth transition in to employment in the Service sector. Toward that objective, Jetson posited both a ‘Switch Point Demand’ function and a ‘Switch Point Supply’ function - akin to Excess Labor Supply & Demand functions:

Jetson modelled the Service Sector as demanding Switch points, SwPtDS; the demand increasing in Service sector Output, Ys, but decreasing in manufacturing wages, wM, and Experience, ExpM, of prospective Manufacturing employees. To factor in family-stage-specific circumstances that obstructed the transition, he included, Dep, representing the number of dependents, as an additional variable (Jetson gulped hard for what it meant in his case). In a similar vein, the Supply of Manufacturing Sector Switch points, SwPtSM increased in wages, wM, and Net Investment, IT, but decreased in own Output, YM. In addition, Jetson added a variable, FD, representing Cumulative FDs subscribed to by Blue collar labor in lieu of wages (Jetson made a mental note to explain later what he meant by his ‘Wage-FD’ strategy). It captured the employer’s proclivity to retain employees willing to sacrifice wages for long-term financial security.

The demand and supply functions specified, Jetson set the ball rolling. He required a pan-industry Labor Organization to minimize the area to the left and below the intersection of the two functions in the SwPt–wM space. The intersection of the SwPt Demand function with the SwPt Supply function (plotted against wM) revealed the optimal Switch Points, SwPt*, below which the Service Sector made ‘Wage-protected’ offers to ‘redundant’ manufacturing employees. The equilibrium SwPt* varied with both Supply and Demand factors, thus lending a touch of uncertainty and cyclicity to the process of Labor migration. The Switch Point strategy facilitated the smooth transfer of Manufacturing labor to the Service Sector while protecting wages, and offered blue-collar labor the opportunity to tune their wages and savings in line with economic and labor-market prospects.

Having designed a mechanism that provided for a smooth adjustment in the Labor market, Jetson chose strategically to aggregate the Blue-collar work force across all Manufacturing industries separate from Service Sector Employees (in which, he included the Manufacturing White Collar employees as well). Next, he bought in to the Blue Collar Pension Fund Authority, PFA, which managed FD contributions as well as the stock purchases and bond assignments to each employee’s portfolio). He intended, given his read of the future, that the Blue-collar PFA would facilitate the implementation of a policy that would, in essence, reduce the wage-rental ratio, w/v, in each sector to that consistent with a robot economy as revealed in the K*, IT*, and L* expressions. In essence, he achieved it by offering wealth compensations to induce voluntary reductions in wages. Each blue-collar employee, whether in Manufacturing or Service Sector, was offered as much in stocks and bonds as the reductions he or she accepted from wages, toward purchase of Long FDs in to his or her pension account. The FDs, and the bundled, matched Stocks/Bonds ensured employees were left at least as well-off in the immediate term, and likely wealthier in the long-run. In this manner, Jetson de-linked wages from work hours, and effectively reduced the wage-rental ratio as it applied to, or, was perceived for operational and investment decisions, thus facilitating a transition to an AI-Robot Economy. Employees too, factored in the wage reduction for their consumption decisions, but made longer term lifestyle decisions based on assets they held with the PFA.

In choosing their Stock compensation for wages ‘sacrificed’ to the future as FDs, Blue collar employees were permitted their choice of stocks between ‘Own firm stock’, a zero-correlation ‘Perpendicular firm stock’ and a broad Stock market Index fund. The Employer, however, deferred the issue of FDs funds; instead it guaranteed ‘Earned Wage Payables, EWP, issued by the PFA. EWPs represented a ‘wages payable’ against the Employer, and listed as an ‘asset’ on PFA books in the sense it was liquid and could be encashed on demand. These EWPs were taken a lien upon by the pan-industry Blue-collar Labor Union, after which the PFA issued FD credits, FDCs (a ‘legal-twist’ that Jetson leveraged for a larger resolution) to the pension accounts of its subscribers.

Yet weary from thinking thru the first part of his proposal, Jetson moved on to the second. Lest the ‘wealth compensation for wage sacrifice’ strategy be presumed a mere re-classification of compensation, and given potential impacts upon various facets of the society, Jetson hastened to unravel a larger resolution for the Robotmation economy. In his resolution, the Fed was an independent agency in charge of ensuring financial stability – a charge that included the management of currency, bank deposits, bullion, interest rates and foreign exchange. Now, the Fed, as part of its duty to ensure financial stability, managed Asset-Liability balance of the economy, with a ‘back of the envelope’ thumb rule:

In the context of his task, Jetson imagined a creative re-interpretation of the above:

The Fed accommodated the demand for currency arising from the growth in Net Assets by either permitting or issuing IPOs/FPOs, issuing FDs or Long Bonds, or by managing its Foreign Currency and Bullion operations. Jetson was no genius, but he found the EWPs (which constituted an ‘earned payable’, a ‘Receivable’ on PFA books, and upon which the FDCs were issued), both an excellent ‘raison d’etre’ and a suitable ‘collateral’ for the issue of new Currency during asset re-balancing operations. By his reckoning, the Fed, rebalanced assets and liabilities around its endogenous instruments – the issue/manipulation of Currency, Bullion, IPO/FPO, Foreign exchange and Long Bonds. Jetson first required that Bullion be adjusted to cancel out changes in the FD and Foreign currency holdings:

Thus cancelled out, the Asset-Liability balance reduced to:

By his 2-step resolution, the Fed on one hand, adjusted its bullion operations to cancel out against foreign exchange and FD(C)s issued, and on the other, issued new Currency to equal the sum of IPO/FPO and Long Bonds issued. The Fed paid for the use of EWPs by ‘sponsoring’ the conversion of FDCs to FDs that were in turn credited in to the accounts of the Blue-collareds at the PFA. The Government ‘bought’ the new issue of Long Bonds from the Fed (or, equivalently, sponsored them), and forwarded them to the PFA toward its match for the participation of employees in the ‘Robotmation scheme’. In addition, the Government strategically bought in to the IPO/FPO so it could recover tax revenues lost from ROE-based tax-credits that it offered to firms when the stock appreciated post the rise in profits following introduction of Robotmation. Compensated, on one hand, with ROE-based tax credits, and relieved of immediately making good on the EWPs, manufacturing firms offered larger discounts on their stocks to their blue-collared employees in their ESOPs to pave the way for robotmation. The discounts, funded by the deferred EWP and limited to FD subscribers, served to further incentivize the participation of the Blue-collared in the ‘Robot Economy’.

Tying the loose ends, Jetson confirmed that his 2-pronged proposal compensated the wage sacrifices made by the Blue-collared labor in anticipation of a Robot economy three ways – FDs, Employer-discounted stocks, and Government-sponsored Long Bonds. Jetson verified that the Blue-collar Union cancelled its lien on the EWPs, and the PFA recovered its FD ‘principal’ – the face value of the EWPs issued – when the Fed ‘sponsored’ the conversion of FDCs to FDs. The Employers leveraged, and made good their deferred FD obligations to the PFA, by funding a discounted Stock offer to participating employees. The Government, too, found it convenient to leverage the issue of Long bonds by the Fed toward its Bond-obligations to the Blue-collar PFA. Further, it found the IPOs/FPOs a convenient asset class to invest in and recover tax revenues lost when those stocks appreciated upon the realization of higher profits following introduction of ‘robotmation’.

The bell rang to alert users the Community College Library closed 6pm sharp. Jetson barely had a minute or two on hand. Hurriedly he scribbled that his 2-pronged solution was of a pareto-nature that benefited all stakeholders – Labor, Capitalists, the Government and the broader society. The three-way compensation to the labor, and the ‘pareto’ nature of adjustments and incentives offered to the Industry and the Government brought about a much faster transition to Robotmation than was considered feasible.

Robotmation was both an opportunity and a threat to humanity’s future. Compensated with wealth accretions, Jetson had eased the Blue-collareds in to an orderly inter-generational transfer to the Robot economy without the mass unemployment and the social strife that had bedevilled other proponents. His resolution, in fact, anticipated and reduced the threat of social discord, while preserving the opportunity of genuine economic gain that a Robot economy offered. His brand of Robonomics was, he felt, particularly appropriate to per-capita-based subsidy economies grappling with a population crisis and a large public sector– a description that fit many emerging nations. But more to his ideals, Jetson believed his proposal was an appropriate transition policy from an inefficient/per-capita, subsidy-based, socialist economy toward a high profit, distributed capital ownership-based, and more efficient Closed Cycle/Robot Economy. It’d interest policy makers and politicians alike for the manner in which it tackled a highly sensitive social issue. The Jetson brand of finance was particularly apt to....

Interrupting himself before he could be shooed away by the library staff, Jetson walked out in to the yet warm late afternoon Sun. As he got to the Chevy, the sun glinting off its windshield, he thought ‘Gotta get the steering fixed soon’.

….. And no day-dreaming on the snaky way back home either!

Thursday, November 3, 2011

Half-Money, Full Sustainability!

Half-Money, Full Sustainability!

Ganga Prasad Rao

http://myprofile.cos.com/gangar

The media was full of news – of the wrong kind. Food colors and flavors poisoning the young yet growing their brains, muscles, and bones (Kidneys are disposable, aren’t they? Hey,…what are stem cells for!). Plastic bags choking every drain, nook and corner of our commons. Detergents with chemicals so toxic they put nuclear materials to shame. Untreated effluents and solid waste despoiling the rivers and our landscape. Industries, caught in the capitalist ‘more profit’ trap, shunning every social responsibility to fulfil the lifestyle expectations of investors abroad. There was no resolution to the problem despite much talk, reams of paper, twitters, blogs, even U-tube videos. Wasn’t anyone smart enough to find a common denominator across these seemingly disparate issues and design a strategy that addressed them together, simultaneously?

Perhaps the media does affect our sensibilities, for an idealist who swore by Justice and was as ‘blue’ as the median on a straight highway, took up the challenge. Much like the mythical Lord Ram, he stepped up to the ‘Bow Challenge’ after his illustrious competitors had failed at it. He realized he’d have to integrate the conflict between equity and efficiency in to his grand ‘externality’ resolution. He appreciated that the resolution must be built around logic, and further, that in-built incentives and dis-incentives were necessary to guarantee the stability of the system. Further, the involvement of the masses and even entrepreneurs would be necessary for his solution to gain any credibility.

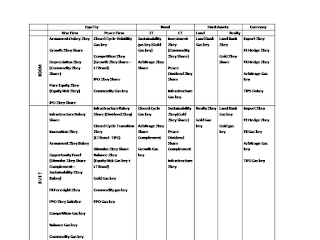

Choosing to depart from the ordinary, the Just Idealist, as he would like to be known (Ego is no sin, or, is it?), declared open membership to, and participation in the ‘Alternate Economy’. He created 3 pots of money, which he christened ‘Equity Half-Money’, EqHM, ‘Efficiency Half-Money’, EfHM and, ExHM, Externality Half-Money. The EqHM pot was the repository of funds meant to stimulate ‘equity’ beyond capitalist consumption. The EfHM, the efficiency analogue of EqHM, served to hold funds meant for investments in firms that enhanced the efficiency of the larger economy. Funds for the EfHM were sourced from Closed-Cycle 2key Bakey, and LT Bonds; the latter being ‘No Diligence’ funds that needed to ensure a ‘Full key’ (a ‘demonstration’ of intentions to be ‘Inefficiency-, Externality- and Inequity Zero’) before entering the Equity markets. The ExHM pot held reserves for firms meant to provide services to correct environmental externalities. The ExHM Money pot was filled by a ‘Green 2key’ plus an ‘Infrastructure Gaskey’. Funds for EqHM were drawn from Gold markets, which were ‘required’ to offer ‘Inequity Utility Compensation’ (and sponsor a ‘Diamond key IPO’) in ‘Equal Opposite’ of those ‘Peace’ firms that had given up and stepped down in Gold Gaskey, short of achieving ‘Diamond’ status. Consistent with the Half-Money Pots, the Just Idealist provided for three types of firms: ‘Equity Services firms’, EqSF, ‘Efficiency Services firms’, EfSF, and ‘Externality Services firms’, ExSF.

Participants in the Alternate Economy, whether a group of individuals, an association, institution, or a firm, that engaged in a pre-approved and pre-announced set of environmentally- and socially-conscious positive acts were issued with uniquely identified ‘Money Points’, and the same was recorded to their credit (not unlike eMoney/MobileMoney). Firms earned Efficiency Points, EfPt and Externality Points, ExPt, in return for providing ‘Efficiency Services’ and ‘Externality Services’ - services not supplied in an Open capitalist economy for want of economic feasibility or regulatory incentives. EfSF firms earned EfPt by engaging in activities as diverse as R&D for more efficient, new technological processes, refining uneconomic non-recyclables, producing environmentally safer, higher quality products, and offering alternative bio-degradable formulations. ExSF firms provided environmental services such as effluent treatment and solid waste management services, for which they were paid in Environmental Points, ExPt. ExSF provided ‘Utility Compensation (UC)’ services and earned Equity Points, EqPt, in return for those services.

To ensure the EfSF and ExSF did not exploit the dedicated money pots, the Just Idealist arranged a ‘See-saw Triangular Balance’ between, on hand, the EqHM-EfHM fund pair and, on the other, the EqHM-ExHM fund pair - the former offering ‘Utility Compensation’, UC, to households to balance the support given to Closed Cycle failures in the equity markets, the burden of which they paid in their purchases. The latter sponsored UE to the masses at large in return for supporting those environmentally imprudent in the equity market. In Boom times, the ExHM sponsored UE to balance the environmental excesses of an overstretched industry even while the EfHM funded Closed-cycle R&D, and cost-cutting technological developments. In Bust, the ExHM funded environmental restoration while the EfHM underwrote UC to households at large. By supporting Closed-Cycle inefficiencies and tolerating environmental excesses in the Real Economy, but providing for compensatory enjoyment, even remedial action in the Alternate Economy, the Just Idealist was able to bring about a quasi-competitive system in which the wrongs of the present were ‘paid for’ as utility compensation in the short run, but corrected physically/economically over the long run.

Individuals or Households earned EqPt in various ways: recycling batteries, motor oil, collecting & depositing ‘un-economic’ plastic and other ‘non-recyclables, buying certified ‘bio-degradable’ goods and certified organic produce, even volunteering in specified citizen/social duties. These Equity points, transferable among members, would serve as the equivalent of free money or tickets, and further, be valid for transacting with participating EqSF businesses/events thru credit/debit cards as well as thru mobile phones. Romantic Getaways, Cruise ship vacations, Concerts, Trekking trips – activities preferred by the youth whose participation was deemed necessary for the success of the program - were offered by EqSF firms, constituted of EqHM debt capital, exclusively to Equity Point holders, in order of declining EqPt balance. However, and to retain or liven up interest and participation among the masses, EqSF firms were permitted to discount EqPt for their services to randomly chosen members using a probability-distribution-based sampling lottery.

With umpteen ways, both consumption-based and by volunteering, to collect EqPt, and as many ways to spend them, an informal price-system developed around them, guiding participants in to optimal consumption choices. In a similar way, the demand for, and supply of various efficiency enhancement and externality abatement services generated transactions that enabled the discovery of implicit shadow value of EfPt and ExPt. The overlap, on one hand, of certain Equity activities with Efficiency activities, and on the other, with Externality activities, permitted the discovery of implicit exchange values between EqPt, EfPt, and ExPt, which in turn enabled the Just Idealist to optimize utility compensation, resource allocation as well as investment and divestment decisions across the entire Alternate Economy.

The funding arrangement for firms constituted of EfHM or ExHM capital explicitly specified that the debt capital be ‘redeemed’ with ‘Whole Money’ – money obtained by pairing Half-moneys of equal value, whether ‘EqPt-EfPt’ or ‘EqPt-ExPt’. Thus paired, ‘Whole Money’ discharged an equal amount of debt on the capital account. He further envisaged that, firms, whether EqSF, EfSF, or ExSF, would have the option to exit the Alternate Economy (or choose to expand with additional debt capital) upon entirely redeeming the debt capital with ‘Whole Money’ capital. For every EfSF or ExSF firm that discharged its debt with Whole Money and graduated in to the Capitalist Economy through an IPO, an EqSF could claim to have paid off its obligations and turn debt-free. The ‘Whole Money’ strategy permitted the Just Idealist to claim that he had indeed brought about a ‘Full key’ resolution to what was ‘tainted money’ - one that would obtain a 3-way balance in the see-saw Alternate Economy, and even gain in the Capitalist Economy.

Enamoured by the prospect of participating in a ‘green’ movement that rewarded participants for their economically and environmentally-conscious choices, even out of turn, the public, particularly the youth, joined in large numbers, providing budding entrepreneurs the consumer base necessary to kickstart their operations. With the availability of easy debt toward the capital for EqSF, EfSF and ExSF, and the opportunity of exploiting a ready market in UC, many entrepreneurs came forward to service the Alternate Economy. The Capitalist Economy and the Alternate Economy served as foils to each other - the former invading upon the latter when environmentally unsustainable, or, less than diligent in its services; the latter encroaching upon the former if they turned monopolistic or inefficient, or tardy in capitalizing on capitalist market opportunities. Between the tug-of-war of the Capitalist-Alternate Economy, and the 3-way see-saw within the Alternate Economy, the markets turned competitive, the society equitable, and the environment sustainable.

As for the ‘Bow Challenge’, the Just Idealist left it to the votes from participants in the Alternate Economy !

Ganga Prasad Rao

http://myprofile.cos.com/gangar

The media was full of news – of the wrong kind. Food colors and flavors poisoning the young yet growing their brains, muscles, and bones (Kidneys are disposable, aren’t they? Hey,…what are stem cells for!). Plastic bags choking every drain, nook and corner of our commons. Detergents with chemicals so toxic they put nuclear materials to shame. Untreated effluents and solid waste despoiling the rivers and our landscape. Industries, caught in the capitalist ‘more profit’ trap, shunning every social responsibility to fulfil the lifestyle expectations of investors abroad. There was no resolution to the problem despite much talk, reams of paper, twitters, blogs, even U-tube videos. Wasn’t anyone smart enough to find a common denominator across these seemingly disparate issues and design a strategy that addressed them together, simultaneously?

Perhaps the media does affect our sensibilities, for an idealist who swore by Justice and was as ‘blue’ as the median on a straight highway, took up the challenge. Much like the mythical Lord Ram, he stepped up to the ‘Bow Challenge’ after his illustrious competitors had failed at it. He realized he’d have to integrate the conflict between equity and efficiency in to his grand ‘externality’ resolution. He appreciated that the resolution must be built around logic, and further, that in-built incentives and dis-incentives were necessary to guarantee the stability of the system. Further, the involvement of the masses and even entrepreneurs would be necessary for his solution to gain any credibility.

Choosing to depart from the ordinary, the Just Idealist, as he would like to be known (Ego is no sin, or, is it?), declared open membership to, and participation in the ‘Alternate Economy’. He created 3 pots of money, which he christened ‘Equity Half-Money’, EqHM, ‘Efficiency Half-Money’, EfHM and, ExHM, Externality Half-Money. The EqHM pot was the repository of funds meant to stimulate ‘equity’ beyond capitalist consumption. The EfHM, the efficiency analogue of EqHM, served to hold funds meant for investments in firms that enhanced the efficiency of the larger economy. Funds for the EfHM were sourced from Closed-Cycle 2key Bakey, and LT Bonds; the latter being ‘No Diligence’ funds that needed to ensure a ‘Full key’ (a ‘demonstration’ of intentions to be ‘Inefficiency-, Externality- and Inequity Zero’) before entering the Equity markets. The ExHM pot held reserves for firms meant to provide services to correct environmental externalities. The ExHM Money pot was filled by a ‘Green 2key’ plus an ‘Infrastructure Gaskey’. Funds for EqHM were drawn from Gold markets, which were ‘required’ to offer ‘Inequity Utility Compensation’ (and sponsor a ‘Diamond key IPO’) in ‘Equal Opposite’ of those ‘Peace’ firms that had given up and stepped down in Gold Gaskey, short of achieving ‘Diamond’ status. Consistent with the Half-Money Pots, the Just Idealist provided for three types of firms: ‘Equity Services firms’, EqSF, ‘Efficiency Services firms’, EfSF, and ‘Externality Services firms’, ExSF.

Participants in the Alternate Economy, whether a group of individuals, an association, institution, or a firm, that engaged in a pre-approved and pre-announced set of environmentally- and socially-conscious positive acts were issued with uniquely identified ‘Money Points’, and the same was recorded to their credit (not unlike eMoney/MobileMoney). Firms earned Efficiency Points, EfPt and Externality Points, ExPt, in return for providing ‘Efficiency Services’ and ‘Externality Services’ - services not supplied in an Open capitalist economy for want of economic feasibility or regulatory incentives. EfSF firms earned EfPt by engaging in activities as diverse as R&D for more efficient, new technological processes, refining uneconomic non-recyclables, producing environmentally safer, higher quality products, and offering alternative bio-degradable formulations. ExSF firms provided environmental services such as effluent treatment and solid waste management services, for which they were paid in Environmental Points, ExPt. ExSF provided ‘Utility Compensation (UC)’ services and earned Equity Points, EqPt, in return for those services.

To ensure the EfSF and ExSF did not exploit the dedicated money pots, the Just Idealist arranged a ‘See-saw Triangular Balance’ between, on hand, the EqHM-EfHM fund pair and, on the other, the EqHM-ExHM fund pair - the former offering ‘Utility Compensation’, UC, to households to balance the support given to Closed Cycle failures in the equity markets, the burden of which they paid in their purchases. The latter sponsored UE to the masses at large in return for supporting those environmentally imprudent in the equity market. In Boom times, the ExHM sponsored UE to balance the environmental excesses of an overstretched industry even while the EfHM funded Closed-cycle R&D, and cost-cutting technological developments. In Bust, the ExHM funded environmental restoration while the EfHM underwrote UC to households at large. By supporting Closed-Cycle inefficiencies and tolerating environmental excesses in the Real Economy, but providing for compensatory enjoyment, even remedial action in the Alternate Economy, the Just Idealist was able to bring about a quasi-competitive system in which the wrongs of the present were ‘paid for’ as utility compensation in the short run, but corrected physically/economically over the long run.

Individuals or Households earned EqPt in various ways: recycling batteries, motor oil, collecting & depositing ‘un-economic’ plastic and other ‘non-recyclables, buying certified ‘bio-degradable’ goods and certified organic produce, even volunteering in specified citizen/social duties. These Equity points, transferable among members, would serve as the equivalent of free money or tickets, and further, be valid for transacting with participating EqSF businesses/events thru credit/debit cards as well as thru mobile phones. Romantic Getaways, Cruise ship vacations, Concerts, Trekking trips – activities preferred by the youth whose participation was deemed necessary for the success of the program - were offered by EqSF firms, constituted of EqHM debt capital, exclusively to Equity Point holders, in order of declining EqPt balance. However, and to retain or liven up interest and participation among the masses, EqSF firms were permitted to discount EqPt for their services to randomly chosen members using a probability-distribution-based sampling lottery.

With umpteen ways, both consumption-based and by volunteering, to collect EqPt, and as many ways to spend them, an informal price-system developed around them, guiding participants in to optimal consumption choices. In a similar way, the demand for, and supply of various efficiency enhancement and externality abatement services generated transactions that enabled the discovery of implicit shadow value of EfPt and ExPt. The overlap, on one hand, of certain Equity activities with Efficiency activities, and on the other, with Externality activities, permitted the discovery of implicit exchange values between EqPt, EfPt, and ExPt, which in turn enabled the Just Idealist to optimize utility compensation, resource allocation as well as investment and divestment decisions across the entire Alternate Economy.

The funding arrangement for firms constituted of EfHM or ExHM capital explicitly specified that the debt capital be ‘redeemed’ with ‘Whole Money’ – money obtained by pairing Half-moneys of equal value, whether ‘EqPt-EfPt’ or ‘EqPt-ExPt’. Thus paired, ‘Whole Money’ discharged an equal amount of debt on the capital account. He further envisaged that, firms, whether EqSF, EfSF, or ExSF, would have the option to exit the Alternate Economy (or choose to expand with additional debt capital) upon entirely redeeming the debt capital with ‘Whole Money’ capital. For every EfSF or ExSF firm that discharged its debt with Whole Money and graduated in to the Capitalist Economy through an IPO, an EqSF could claim to have paid off its obligations and turn debt-free. The ‘Whole Money’ strategy permitted the Just Idealist to claim that he had indeed brought about a ‘Full key’ resolution to what was ‘tainted money’ - one that would obtain a 3-way balance in the see-saw Alternate Economy, and even gain in the Capitalist Economy.

Enamoured by the prospect of participating in a ‘green’ movement that rewarded participants for their economically and environmentally-conscious choices, even out of turn, the public, particularly the youth, joined in large numbers, providing budding entrepreneurs the consumer base necessary to kickstart their operations. With the availability of easy debt toward the capital for EqSF, EfSF and ExSF, and the opportunity of exploiting a ready market in UC, many entrepreneurs came forward to service the Alternate Economy. The Capitalist Economy and the Alternate Economy served as foils to each other - the former invading upon the latter when environmentally unsustainable, or, less than diligent in its services; the latter encroaching upon the former if they turned monopolistic or inefficient, or tardy in capitalizing on capitalist market opportunities. Between the tug-of-war of the Capitalist-Alternate Economy, and the 3-way see-saw within the Alternate Economy, the markets turned competitive, the society equitable, and the environment sustainable.

As for the ‘Bow Challenge’, the Just Idealist left it to the votes from participants in the Alternate Economy !

Tuesday, November 1, 2011

'Boursing' My Way to Utopia !

Boursing My Way to Utopia !

Ganga Prasad G. Rao

http://myprofile.cos.com/gangar

….And Alice woke up, all blurry-eyed, not remembering a word of what she had penned while in Wonderland. After staring and blinking a few seconds, she dozed off again in to another dream, this time just as exotic. Yes, something wasvery ‘grotesque’. The entire global financial system was in disarray. Panic ruled the markets.Buffeted between fears of currency crisis, global depression, and sovereign default, the entire financial community was looking for deliverance from their Messiah. But would the Messiah deliver on their pleas?

Call it the Big Lord’s design, Satan’s test of character, or cruel fate, but the Messiah was none other than a half-baked, unemployed albeit worldly-wise Economist, who, oblivious to the utter desperation in the financial community, fancied his hand at putting the world in order, and blog his resolution to the travails of the global markets. And, pray, what was his message? The Messiah accepted the fallacies of the past world, but stood resolute in his vision of the future - a world in which the sins, omissions and commissions of the industry were addressed in an overt, balanced, flexible and comprehensiveway. Rather than focus on any one externality to the exclusion of other significant externalities, the Messiah proposedclubbing them together in to an aggregate measure of firm-level externality. Firms as diverse as power plants burning brown coal, armaments industry overstocking mines, missiles and grenades to sustain employment, mining, refining and shipping, and the pesticide industries preferring environment-damaging inorganic pesticides to safer organic alternatives, could pay off their residual, un-mitigated externality, whether associated with inputs, outputs, transportation, consumption or disposal, in the capital market.

The Messiah’s disciple wondered what theory, principles, or tenets underlay the claim to measure aggregate non-pecuniary externality, and how he would go about extracting it. Perhaps it was telepathy, perhaps the Messiah was in the mood to sermonize; regardless, he chose to reveal his logic. Short of claiming the Garden of Eden as his vision of Sustainability, the Messiah advised that no matter how wrong the world was in the present, it should turn sustainable at some future point in time. And if the roots of the current unsustainability could be traced to the industry, the seeds of sustainability too lay in reforming the industry. Since the equity markets typically operated with limited foresight, the burden of sustainability fell upon the bond market. It was by issuing long bonds to correct wrongs of the past that the Government turned the future sustainable (and financed its budget in the present). Greater the wrong, the more long bonds issued to fund remedial action across years, even decades (Fukushima?, Why does it ring a bell?). Thus, the quantumof, and price variations in the long term bond market gave an indication of the extent of the ‘externality’ outstanding. The Messiah simply ensured a balance between theexternality damages by the industry and the value of outstanding long bonds. It was by perturbing the balance while simulating a firm as a monopoly that he comprehensively gauged the magnitude of its externalities. These externalities were distributed among shares and traded away in a ‘paired-complement’ strategy by creating two externality-differentiated share and bond classes.

Despite his misgivings of correcting externalities by monetary means in an inequitable world (which pre-supposed, among other things, an efficient capital market, in particular a comprehensive Sustainability Index feeding in to Long Bond pricing formula), the Messiah went about his mission methodically. He firstcreated some terminology: an economy was comprised of ‘War Firms’ and ‘Peace Firms’. Firms that truly believed in sustainable production and manufacturing, regardless of how polluting or non-polluting their process was, were assigned the ‘Peace’ label. Hawkish firms that would rather generate excess, short-term profits than go the extra mile for sustainability were deemed ‘War’ firms. To denote the extent of potential gains in various market sections, he coined ‘ungodly’ phrases: ‘2key’, signifying large and immediate, if not ‘excess returns’ (the all too familiar ‘alpha’) as appropriate to the asset class, and ‘gas key’, denoting nominal returns, if at all. In between these extremes, he recognized ‘Bakey’ (residual), ‘Complements’ and ‘Shares’ (and an ‘Ookey’ was short for ‘You should know better’!). These constituted the various fractions of every pot of money no matter which asset class – whether equity, commodity, bond, gold, or realty. The 2key portion rewarded firms for meeting objective measures of achievement; the ‘Gas key’ was essentially a ‘Capital Protection Fund’ that provided funds to alleviate ‘performance deficiencies’in stock market firms if by merely adding volatility to those market sections. (It protected the sponsors’ capital while leveraging the short-term gains of speculators to cause volatility in the equity market). Consistent with the theme of his mission, the Messiah distinguished between ‘Externality Outstanding’, EO equity shares and ‘Externality Internalized’, EI shares.