Half-Money, Full Sustainability!

Ganga Prasad Rao

http://myprofile.cos.com/gangar

The media was full of news – of the wrong kind. Food colors and flavors poisoning the young yet growing their brains, muscles, and bones (Kidneys are disposable, aren’t they? Hey,…what are stem cells for!). Plastic bags choking every drain, nook and corner of our commons. Detergents with chemicals so toxic they put nuclear materials to shame. Untreated effluents and solid waste despoiling the rivers and our landscape. Industries, caught in the capitalist ‘more profit’ trap, shunning every social responsibility to fulfil the lifestyle expectations of investors abroad. There was no resolution to the problem despite much talk, reams of paper, twitters, blogs, even U-tube videos. Wasn’t anyone smart enough to find a common denominator across these seemingly disparate issues and design a strategy that addressed them together, simultaneously?

Perhaps the media does affect our sensibilities, for an idealist who swore by Justice and was as ‘blue’ as the median on a straight highway, took up the challenge. Much like the mythical Lord Ram, he stepped up to the ‘Bow Challenge’ after his illustrious competitors had failed at it. He realized he’d have to integrate the conflict between equity and efficiency in to his grand ‘externality’ resolution. He appreciated that the resolution must be built around logic, and further, that in-built incentives and dis-incentives were necessary to guarantee the stability of the system. Further, the involvement of the masses and even entrepreneurs would be necessary for his solution to gain any credibility.

Choosing to depart from the ordinary, the Just Idealist, as he would like to be known (Ego is no sin, or, is it?), declared open membership to, and participation in the ‘Alternate Economy’. He created 3 pots of money, which he christened ‘Equity Half-Money’, EqHM, ‘Efficiency Half-Money’, EfHM and, ExHM, Externality Half-Money. The EqHM pot was the repository of funds meant to stimulate ‘equity’ beyond capitalist consumption. The EfHM, the efficiency analogue of EqHM, served to hold funds meant for investments in firms that enhanced the efficiency of the larger economy. Funds for the EfHM were sourced from Closed-Cycle 2key Bakey, and LT Bonds; the latter being ‘No Diligence’ funds that needed to ensure a ‘Full key’ (a ‘demonstration’ of intentions to be ‘Inefficiency-, Externality- and Inequity Zero’) before entering the Equity markets. The ExHM pot held reserves for firms meant to provide services to correct environmental externalities. The ExHM Money pot was filled by a ‘Green 2key’ plus an ‘Infrastructure Gaskey’. Funds for EqHM were drawn from Gold markets, which were ‘required’ to offer ‘Inequity Utility Compensation’ (and sponsor a ‘Diamond key IPO’) in ‘Equal Opposite’ of those ‘Peace’ firms that had given up and stepped down in Gold Gaskey, short of achieving ‘Diamond’ status. Consistent with the Half-Money Pots, the Just Idealist provided for three types of firms: ‘Equity Services firms’, EqSF, ‘Efficiency Services firms’, EfSF, and ‘Externality Services firms’, ExSF.

Participants in the Alternate Economy, whether a group of individuals, an association, institution, or a firm, that engaged in a pre-approved and pre-announced set of environmentally- and socially-conscious positive acts were issued with uniquely identified ‘Money Points’, and the same was recorded to their credit (not unlike eMoney/MobileMoney). Firms earned Efficiency Points, EfPt and Externality Points, ExPt, in return for providing ‘Efficiency Services’ and ‘Externality Services’ - services not supplied in an Open capitalist economy for want of economic feasibility or regulatory incentives. EfSF firms earned EfPt by engaging in activities as diverse as R&D for more efficient, new technological processes, refining uneconomic non-recyclables, producing environmentally safer, higher quality products, and offering alternative bio-degradable formulations. ExSF firms provided environmental services such as effluent treatment and solid waste management services, for which they were paid in Environmental Points, ExPt. ExSF provided ‘Utility Compensation (UC)’ services and earned Equity Points, EqPt, in return for those services.

To ensure the EfSF and ExSF did not exploit the dedicated money pots, the Just Idealist arranged a ‘See-saw Triangular Balance’ between, on hand, the EqHM-EfHM fund pair and, on the other, the EqHM-ExHM fund pair - the former offering ‘Utility Compensation’, UC, to households to balance the support given to Closed Cycle failures in the equity markets, the burden of which they paid in their purchases. The latter sponsored UE to the masses at large in return for supporting those environmentally imprudent in the equity market. In Boom times, the ExHM sponsored UE to balance the environmental excesses of an overstretched industry even while the EfHM funded Closed-cycle R&D, and cost-cutting technological developments. In Bust, the ExHM funded environmental restoration while the EfHM underwrote UC to households at large. By supporting Closed-Cycle inefficiencies and tolerating environmental excesses in the Real Economy, but providing for compensatory enjoyment, even remedial action in the Alternate Economy, the Just Idealist was able to bring about a quasi-competitive system in which the wrongs of the present were ‘paid for’ as utility compensation in the short run, but corrected physically/economically over the long run.

Individuals or Households earned EqPt in various ways: recycling batteries, motor oil, collecting & depositing ‘un-economic’ plastic and other ‘non-recyclables, buying certified ‘bio-degradable’ goods and certified organic produce, even volunteering in specified citizen/social duties. These Equity points, transferable among members, would serve as the equivalent of free money or tickets, and further, be valid for transacting with participating EqSF businesses/events thru credit/debit cards as well as thru mobile phones. Romantic Getaways, Cruise ship vacations, Concerts, Trekking trips – activities preferred by the youth whose participation was deemed necessary for the success of the program - were offered by EqSF firms, constituted of EqHM debt capital, exclusively to Equity Point holders, in order of declining EqPt balance. However, and to retain or liven up interest and participation among the masses, EqSF firms were permitted to discount EqPt for their services to randomly chosen members using a probability-distribution-based sampling lottery.

With umpteen ways, both consumption-based and by volunteering, to collect EqPt, and as many ways to spend them, an informal price-system developed around them, guiding participants in to optimal consumption choices. In a similar way, the demand for, and supply of various efficiency enhancement and externality abatement services generated transactions that enabled the discovery of implicit shadow value of EfPt and ExPt. The overlap, on one hand, of certain Equity activities with Efficiency activities, and on the other, with Externality activities, permitted the discovery of implicit exchange values between EqPt, EfPt, and ExPt, which in turn enabled the Just Idealist to optimize utility compensation, resource allocation as well as investment and divestment decisions across the entire Alternate Economy.

The funding arrangement for firms constituted of EfHM or ExHM capital explicitly specified that the debt capital be ‘redeemed’ with ‘Whole Money’ – money obtained by pairing Half-moneys of equal value, whether ‘EqPt-EfPt’ or ‘EqPt-ExPt’. Thus paired, ‘Whole Money’ discharged an equal amount of debt on the capital account. He further envisaged that, firms, whether EqSF, EfSF, or ExSF, would have the option to exit the Alternate Economy (or choose to expand with additional debt capital) upon entirely redeeming the debt capital with ‘Whole Money’ capital. For every EfSF or ExSF firm that discharged its debt with Whole Money and graduated in to the Capitalist Economy through an IPO, an EqSF could claim to have paid off its obligations and turn debt-free. The ‘Whole Money’ strategy permitted the Just Idealist to claim that he had indeed brought about a ‘Full key’ resolution to what was ‘tainted money’ - one that would obtain a 3-way balance in the see-saw Alternate Economy, and even gain in the Capitalist Economy.

Enamoured by the prospect of participating in a ‘green’ movement that rewarded participants for their economically and environmentally-conscious choices, even out of turn, the public, particularly the youth, joined in large numbers, providing budding entrepreneurs the consumer base necessary to kickstart their operations. With the availability of easy debt toward the capital for EqSF, EfSF and ExSF, and the opportunity of exploiting a ready market in UC, many entrepreneurs came forward to service the Alternate Economy. The Capitalist Economy and the Alternate Economy served as foils to each other - the former invading upon the latter when environmentally unsustainable, or, less than diligent in its services; the latter encroaching upon the former if they turned monopolistic or inefficient, or tardy in capitalizing on capitalist market opportunities. Between the tug-of-war of the Capitalist-Alternate Economy, and the 3-way see-saw within the Alternate Economy, the markets turned competitive, the society equitable, and the environment sustainable.

As for the ‘Bow Challenge’, the Just Idealist left it to the votes from participants in the Alternate Economy !

Thursday, November 3, 2011

Tuesday, November 1, 2011

'Boursing' My Way to Utopia !

Boursing My Way to Utopia !

Ganga Prasad G. Rao

http://myprofile.cos.com/gangar

….And Alice woke up, all blurry-eyed, not remembering a word of what she had penned while in Wonderland. After staring and blinking a few seconds, she dozed off again in to another dream, this time just as exotic. Yes, something wasvery ‘grotesque’. The entire global financial system was in disarray. Panic ruled the markets.Buffeted between fears of currency crisis, global depression, and sovereign default, the entire financial community was looking for deliverance from their Messiah. But would the Messiah deliver on their pleas?

Call it the Big Lord’s design, Satan’s test of character, or cruel fate, but the Messiah was none other than a half-baked, unemployed albeit worldly-wise Economist, who, oblivious to the utter desperation in the financial community, fancied his hand at putting the world in order, and blog his resolution to the travails of the global markets. And, pray, what was his message? The Messiah accepted the fallacies of the past world, but stood resolute in his vision of the future - a world in which the sins, omissions and commissions of the industry were addressed in an overt, balanced, flexible and comprehensiveway. Rather than focus on any one externality to the exclusion of other significant externalities, the Messiah proposedclubbing them together in to an aggregate measure of firm-level externality. Firms as diverse as power plants burning brown coal, armaments industry overstocking mines, missiles and grenades to sustain employment, mining, refining and shipping, and the pesticide industries preferring environment-damaging inorganic pesticides to safer organic alternatives, could pay off their residual, un-mitigated externality, whether associated with inputs, outputs, transportation, consumption or disposal, in the capital market.

The Messiah’s disciple wondered what theory, principles, or tenets underlay the claim to measure aggregate non-pecuniary externality, and how he would go about extracting it. Perhaps it was telepathy, perhaps the Messiah was in the mood to sermonize; regardless, he chose to reveal his logic. Short of claiming the Garden of Eden as his vision of Sustainability, the Messiah advised that no matter how wrong the world was in the present, it should turn sustainable at some future point in time. And if the roots of the current unsustainability could be traced to the industry, the seeds of sustainability too lay in reforming the industry. Since the equity markets typically operated with limited foresight, the burden of sustainability fell upon the bond market. It was by issuing long bonds to correct wrongs of the past that the Government turned the future sustainable (and financed its budget in the present). Greater the wrong, the more long bonds issued to fund remedial action across years, even decades (Fukushima?, Why does it ring a bell?). Thus, the quantumof, and price variations in the long term bond market gave an indication of the extent of the ‘externality’ outstanding. The Messiah simply ensured a balance between theexternality damages by the industry and the value of outstanding long bonds. It was by perturbing the balance while simulating a firm as a monopoly that he comprehensively gauged the magnitude of its externalities. These externalities were distributed among shares and traded away in a ‘paired-complement’ strategy by creating two externality-differentiated share and bond classes.

Despite his misgivings of correcting externalities by monetary means in an inequitable world (which pre-supposed, among other things, an efficient capital market, in particular a comprehensive Sustainability Index feeding in to Long Bond pricing formula), the Messiah went about his mission methodically. He firstcreated some terminology: an economy was comprised of ‘War Firms’ and ‘Peace Firms’. Firms that truly believed in sustainable production and manufacturing, regardless of how polluting or non-polluting their process was, were assigned the ‘Peace’ label. Hawkish firms that would rather generate excess, short-term profits than go the extra mile for sustainability were deemed ‘War’ firms. To denote the extent of potential gains in various market sections, he coined ‘ungodly’ phrases: ‘2key’, signifying large and immediate, if not ‘excess returns’ (the all too familiar ‘alpha’) as appropriate to the asset class, and ‘gas key’, denoting nominal returns, if at all. In between these extremes, he recognized ‘Bakey’ (residual), ‘Complements’ and ‘Shares’ (and an ‘Ookey’ was short for ‘You should know better’!). These constituted the various fractions of every pot of money no matter which asset class – whether equity, commodity, bond, gold, or realty. The 2key portion rewarded firms for meeting objective measures of achievement; the ‘Gas key’ was essentially a ‘Capital Protection Fund’ that provided funds to alleviate ‘performance deficiencies’in stock market firms if by merely adding volatility to those market sections. (It protected the sponsors’ capital while leveraging the short-term gains of speculators to cause volatility in the equity market). Consistent with the theme of his mission, the Messiah distinguished between ‘Externality Outstanding’, EO equity shares and ‘Externality Internalized’, EI shares.

In the next step, he conceptualized an ‘Externality Quotient’, EQ, acomprehensive externality measure representing the discounted inter-temporal monetary negative,non-pecuniary externalities as normalized by the outstanding equity base of the firm or industry. A pre-market session was designed to elicit the EQ, first for the benchmark ‘EI Equal Frontrunner’ firm (a technological and environmental leader), and then for other firms in the industry/sub-aggregate. After noting the initial ‘equilibrium’ equity and bond prices, the ‘Frontrunner Benchmark’, the Messiah ordered the simulation of each firm by projecting it as a monopoly firm operating at competitive aggregate industry price and output against a designated bundle of long-term bonds of value equal the aggregate equity base of the sector to which the firm belonged. The simulation induced a change in Sustainability indices to the extent the firm’s externalities differed from the Frontrunner Benchmark.The change in the price of the long bond bundle, post simulation, from its benchmark value due changes in the underlying environmental and sustainability indices of the long-bond pricing formula were noted. The projected Gross EQ of the monopoly was simply the change in the value of bonds relative to the ‘Frontrunner Firm’ benchmark. To obtain the net firm EQ, the Gross EQ was re-computed and re-denominated to reflect the firm’s capacity/equity share in the aggregate. That externality estimate was distributed across the utility’s base of equity shares as ‘Sustainability Deficit’, SD. Each SD-tagged equity share now represented a share in the assets and profit stream of the firm, as well as a share in the uncompensated, non-pecuniary externality liability it generated across space and time.

To ensure changes in price of long ‘SD’ bonds indeed measured an externality impact in the pre-open session, the Messiah insisted that a ‘Sustainability Index’, a Divisia index of underlying indicators, factor into LT Bond prices the impact of firm operation on EHS measures in the short, medium and long run. The indicators were chosen to represent various potential and significant damage classes. The sustainability indicators included factors as diverse as air, water and land pollution measures, as well as population, health and social indicators such as maternal and infant mortality, longevity, even violence and terrorism. These measures and indicators were themselves the outputs of underlying scientific, socio-economic and statistical models – measures that had real societal values attached to them but were not priced in to the products and equity shares. The Divisia module, equivalent to a reduced form of an externality costing model, indicated the change in long bond prices for various values of underlying determinants.

The SD-tagged ‘Externality-Outstanding’ (EO) equity share‘entitled’ the firm to generate a certain amount of externality in the course of its business. Every EO-EI share transaction in the equity market released an SD to the bond market where it was bid up or down and priced in to a longbond transaction, again of the same value as the equity transaction. Only upon the cancellation of the Equity SD-ticket in the bond market was an EO equity share converted to ‘Externality-Internalised’ EI share. The Messiah requiredevery ‘EO-EI-SD-ticket’ transaction in the ‘War Zone’ be matched by a ‘Sustainability Complement’ transaction involving a ‘Peace firm’. Thus, 2 SD-tickets were generated simultaneously from the equity market and transferred to the bond market for price-discovery and to sanctify the conversion of Long SD Bonds to SB status.

Anticipating the impracticability of every firm negotiating the bidding of its SD-ticket in the bond market, a recognized haven of the Greens, the Messiah willed a ‘Blue Optimism’ fund and ‘Green Caution fund’. The two funds took opposing positions in the Bond market and competed with other interests in the race to garner as many SD-tickets as possible. The winner - the side which converted all its outstanding SD bonds to SB and prematurely retired the bonds - qualified for a Closed-Cycle IPO 2key; the loser sponsored a ‘De-listing Bakey’. Between them, the bond funds brought about a slow replacement of ‘low dividend yield’ funds with new Closed-cycle ‘growth’ funds that enlivened the market with Growth 2key.

To hasten the transition to an ‘Externality-Internalized’ industry, the Messiah suggested a ‘virtual bifurcation’ of the stock market between the two share classes- EO and EI, the intent being to restrict certain funds and money pots to appropriate share classes.Lest there be a stampede overnight, only the ‘strictly 2key’ money pots – Growth, Opportunity, and Foresight 2keys - were restricted to the EI-section of the market, while the EO section was satisficed with Bakey, Shares, Complements and Gas keys. The Messiah’s ‘bifurcation’ induced promoters and shareholders to churn their shares from EO to EI earlier than they would otherwise, and brought about an early and comprehensive internalization of externalities. This churning of EO shares in to EI shares continued until the entire equity share base turned ‘EI’, and all bonds ‘SB’. At this point, the Messiah deemed the stock market to have ‘soft-landed’ and hailed the birth of an operating, albeit rudimentary, financially closed-cycle economy.

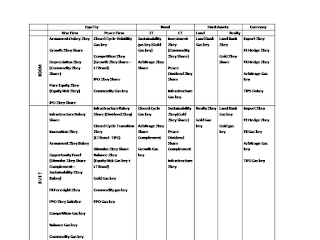

2key: Up to 95%; Share: 40-60%; Complement: 10-40%; Bakey: Residual, Gas key: 0-10% of ‘normal’ returns in asset class.

Now, the traders in the pit, the UPennFund managers on Wall Street,and Chicago Macro-economists pursuing their profession in the rarefied spaces of sky-high towers,alike,were in a tizzy as to how the system would adapt to the various stages of the macro-economic cycle. Once again, they approached the Messiah seeking his distilled essence. The Messiah obliged them, yet again. For each industry group, he used the pre-market session to obtain an estimate of the gross outstanding externality. He instructed the firms take sides – either ‘Peace’ or ‘War’ firms as appropriate to each. He then categorized investible funds in to ‘functional groups’: Growth, Risk Equity, Competition, Sustainable Development, Investment, Innovation, IPO, FPO– to name a few. Finally, lo and behold, the Messiah cranked up his ‘Mensa Economy'.

Boom time it was. Commodity prices spiralled up as the economy hummed and short-term interest rates firmed up. Equity prices, in particular those of ‘War’ and ‘Peace’ EO shares, gained traction. Shareholders in ‘War’ firms were beneficiaries of equity returns that were in consonance with the risk they had borne (Equity Risk 2Key). These firms also reaped rewards from a Commodity 2key Share - a return that supported Capital Retirement if in a Zero-sum with an Investment 2key in Long bonds.Peace firms, however, could only lay claim to a lesser return, a Growth 2key net of any inflation-induced bond impacts (a ‘paired fund’ return maximized by competition, hence Competition 2key). Both ‘War’ and ‘Peace’ firms shared in (own sector) IPO 2key in this phase of the economic cycle.

In the bond market, the Blue Optimism Fund exploited the low bond prices during the equity boom to buyback or exit SD-bonds while converting them to SB status by bidding away SD-tickets available at a discount from the equity market. The buyback enabled the Blue Optimism Fund to prematurely retire bonds, and facilitated the sponsoring of an IPO in the Equity market.

As the Economy peaked and entered the Bust cycle, shareholders in War firms enjoyed the Innovation 2key – a fund meant to support frontier, leading edge research. Both War and Peace firms enjoyed the Bakey returns of an Infrastructure investment fund whose primary gains went to LT Bonds. War firms were also favoured by an FII (Foresight) 2key, meant to pick winners for the early bird investor, andthe FPO 2key Satisfice, a strategic, thinly-disguised Monopoly fund, meant to expand market share by luring investors when most susceptible. These firms also benefited from a ‘paired Opportunity fund’ – a Stimulus 2key net of a Sustainability Bakey. Consistent with the Government’s view, the Opportunity fund ensured any gainaccruing to unsustainable War firms during the Bust period was ephemeral.

The story with ‘Peace Firms’ in Bust was quite different. Having accepted the vision of a sustainable industry, promoters and shareholders relied, on one hand,on the Infrastructure Bakey and a paired ‘Closed-cycle Transition 2key–TIPS’ fund, and on the other, on a paired ‘Balance2key’for equity gains. The Closed Cycle Transition ‘2key’ was essentially long bond returns net of inflation, a 2key maximized by a peaceful and cost-cutting, ‘Full Cost’ competitive economy. The Balance 2key, sourced from Equity Risk remnants (Gas key) and rising Long Bond returns, contributed to returns in this cycle, as did an Infrastructure Bakey camouflaged as Dividend 2key. In Bust, Long bonds attracted an Infrastructure 2key, a Sustainability 2key supported by excess Gold returns (Gold 2key), an Arbitrage 2key from equity and currency markets, and nominally, some Closed Cycle funds to enable aspiring firms to weather the ‘winter’. The Capital Protection Fund, CPF, (a Gold Gas key and a Commodity Gas key) preserved gains from Gold and Commodity markets among Peace firms while sowing the seed for a future 2key return. The Green Caution Fund exercised its option to bid up SD-tickets with the proceeds of its redemption from Long bonds from Peace firms even while investing in them on the equity side of the market.

In the ‘Hard Assets’ category – Land and Realty, the Messiahtrudged the simpler path.A Realty 2key supported Land prices during Bust period, while a Land Bank 2key and a Gold 2key Complement underwrote gains in Realty prices during Boom. A Land Bank gas key supported land assets in Boom, and realty assets in Bust. A Gold gas key added to Volatility in the Realty assets during Bust.

And as far as Currency markets were concerned, the Boom period was characterized by 2keys from Exports, Foreign Exchange Hedge, and FII Hedge pots. In the Bust cycle, currency markets moved with an Import 2key, and Foreign Exchange Hedge key, supplemented by FII gas key and Export gas key. A TIPS fund was distributed in 2key and gas key between the Boom and Bust cycles, albeit with a sting in the tail.

Having discussed threadbare the ideal operation of the stock market, the Messiah, sought to reinforce its utility by mentally simulating a policy goal to eliminate or minimize the Armament industry.He firmly believed that an industry as ‘bad’ and one as close to the government and its secrets as the Armament industry, would survive and proliferate, even if it meant the destruction of nations and their economies. The Messiah’s dilemma was how he would put an end to the scourge that robbed the global citizen of bread on his plate and returns in the market? How would he wind up an industry that had a long record of engendering technical innovations that bolstered the productivity and efficiency of industrially advanced nations, created business opportunities and sustained jobs – the very measures by which the Government and politicians were judged by the electorate? Could he not just give the industry the Christmas week and bull-doze the factories for bread lines come January 1? If the Messiah was no simpleton with child-like innocence camouflaging ignorance, thanks were in order to the Big Lord!

But seriously, the Messiah was aware, that behind the various wars and factional strife, was a coterie of advanced nations and industry barons heavily invested in mining and basic metal firms, in technology supporting those industries, as well as in commodity markets transacting the outputs of those industries. Fact of matter, the Messiah was so wise that he had a downright ‘unholy’suspicion: Could it be that the stakeholders and investors in those industries were forced to resort even to war to recover their investments that had been eroded by the umpteen stock market speculator-day traders? Perhaps Governments that had promised a 100% ‘Total return’ in the capital market to Hard Rock Mining and Basic Metal Industry, HRMBM firms, were obliged to consider novel ways - war and ‘peace-missions’ - to keep them, even if it meant the world was a last few steps away from a WW-III Armageddon?

Fearing the worst, the Messiah came up with a two-pronged ‘Carrot and Stick’ strategy. He decided he would, on one hand, offer the HRMBM industry a reasonable return for the risks they endured by sponsoring a ‘Stimulus 2key’ that stimulated economic demand and raised the standard of living of his followers, and on the other, simultaneously offer the armament industry an incentive to ‘downsize’, an opportunity to innovate in to a ‘non-military’ firm, and an opportunity to generate a ‘peace’ return on its investment while refraining from weapon production. To keep incentives straight, the Messiah exploited differences in intentions and outcomes between the two industries to promote a third party, Agriculture.

To facilitate the realization of the policy goal, the Messiah paired the Armament industry with the HRMBM industry, pitted them against ‘Peace Hawks’ (International Organizations) and Agriculture interests in the Bond market, and initiated equity trading in a ‘bifurcated’ stock market. In the boom-time economy, a Promoter of the Armament ‘War’ firm holding EO shares sought 2keys to realize capital gains, but was denied the same from lack of EI status. Unable to realize capital appreciation, his options were either to lobby and induce foreign policy mis-steps that enabled him to secure armament orders and exploit the Armament 2key, or fold in and submit his shares to the EO-EI conversion program. Sanity and good-will prevailed, and the Armament industry weighed its Externality Quotient in the pre-market session with intention to convert all EO shares to EI status, if eventually. As if walking a balance beam, the promoter sought to optimize, on one hand, the harvesting of 2key returns by releasing as many EO shares to the market as possible without compromising on share price, and on the other, minimize the loss of capital appreciation in the EI side of the Equity market from a delay in offering EO shares to the market. Avoiding the Armament 2key trap, he sold his EO shares to realize a ‘Depreciation2key’ with which to retire Armament production lines. The Buyer was an International Organization that monitored International military relations and managed a Peace Dividend fund. The transaction triggered an ‘SD Complement’ in the ‘Peace zone’ and an SD-ticket in the Bond market. An HRMBM ‘Peace’ firm pounced on the SD Complement and executed a similar trade to realize a ‘Competition 2key’.

Following the equity market transactions, the Bond market announced 2 SD tickets – one each from the Armament firm and the other from the HRMBM firm (both with a floor price supported by the UN/GEF/WWF). The SDs were bid up to different extents by bond market participants. The Armament SD, prized for the large risk to international peace that the industry had caused, was, again, bid away by the Peace Hawk whoapplied ‘Peace Dividend’ funds to buy in to the Bond market (which rose with infusion of the Peace Dividend 2key Share), thus ensuring a presence on both sides of the market. The HRMBM SD, comprised largely of damages to soil and ground water, was of particular interest to NABARD whose mission it was to support agriculture and which had issued agricultural bonds. It bid up the ‘exernality sin’ manifest in the SD tickets and won the right to retire the bonds prematurely when it had ‘redeemed’ sufficient number of SD tickets representing EO shares of value equal outstanding bonds in the market. The NABARD used the proceeds of the prematurely retired bonds to buy in to Land for agricultural use, thus offering a Land 2key to those invested in the asset.

In the Bust cycle, the Armament War firm had many takers for its EO shares. Shareholders had a choice between a Stimulus 2key, Innovation Funds, and Opportunity funds when offloading shares in the market. The Stimulus 2key supported Armament firms to the extent their output served non-military purposes. The Innovation 2key supported strategic research, albeit not necessarily peaceful or ‘Closed cycle’. Thus, the International Organization found it to its advantage to support the Armament firm with an Innovation 2key, and, simultaneously, buy out the SD ticket to consolidate in or exit the Bond Market. The Messiah also offered an Armament 2key, itself a Zero Sum with the Peace Dividend 2key, but only in Bakey, and only to holders of the Armament firm’s EI shares. The strategy restricted capital appreciation and ‘alpha’ to those Armament firms that had substantially converted their share base over to EI status and those that abjured the War route to profits.

The unconverted HRMBM Peace Firm EO shares, besides attracting Stimulus funds, found buyers in Closed Cycle proponents and Balance funds – the former seeking profits from lower cost consequent to enhancing the efficiency of material balances in the firm’s production process, and the latter seeking to profit from correcting the inefficient use of mining and refining capacity for production and stockpiling of arms.

In subsequent cycles, a dominant shareholder in the Armament industry, perhaps a Promoter, secured both the Armament 2key bakey for refraining from Armament production and stockpiling, and a Capital Depreciation/Retirement 2key for his ‘War EO’ shares (The Depreciation 2key was a Zero-Sum with an Investment 2key, both of which were sourced from returns generated in the Commodity market). The Capital Depreciation/Retirement2key was secured from a Peace Dividend Bond foreclosed by bidding away Armament SD-tickets in the bond market (which enabled the Promoter to claim EI status for his shares, a pre-requisite to de-commission an Armament production line or factory). The de-commissioning of Armament factory and/or the reduction in armament stockpile reduced the risk of war, which was an important factor in determining long bond prices. The consequent increase in bond prices was a reward to the Institution sponsoring the Peace Dividend Fund. The churning of the Armament EO to EI shares, induced a similar churn in the HRMBM shares, purchasing the SD-tickets from which enabled NABARD to retire its Agriculture bonds and channel them to purchase land for agricultural use – perhaps a harbinger of a nascent green revolution.

Armament factories outta business, sustained profits for metal and mining industry, a resurgent agriculture sector, an environmentally sustainable industry, and a financially-closed capital market? One would be excused for congratulating the Messiah for showing the path to sustainability, if not salvation. But the Messiah cared not to learn if his followers were ingrates. For, as he trudged his lonely path to the setting sun, he was wise to the nefarious, grand designs of those un-named bent on exploiting the opportunities and loopholes in his proposal and get the better of God in his own paradise (even if it meant a parallel, underground stock market and 8-figure signing bonuses for fresh Ivy League graduates !)

Ganga Prasad G. Rao

http://myprofile.cos.com/gangar

….And Alice woke up, all blurry-eyed, not remembering a word of what she had penned while in Wonderland. After staring and blinking a few seconds, she dozed off again in to another dream, this time just as exotic. Yes, something wasvery ‘grotesque’. The entire global financial system was in disarray. Panic ruled the markets.Buffeted between fears of currency crisis, global depression, and sovereign default, the entire financial community was looking for deliverance from their Messiah. But would the Messiah deliver on their pleas?

Call it the Big Lord’s design, Satan’s test of character, or cruel fate, but the Messiah was none other than a half-baked, unemployed albeit worldly-wise Economist, who, oblivious to the utter desperation in the financial community, fancied his hand at putting the world in order, and blog his resolution to the travails of the global markets. And, pray, what was his message? The Messiah accepted the fallacies of the past world, but stood resolute in his vision of the future - a world in which the sins, omissions and commissions of the industry were addressed in an overt, balanced, flexible and comprehensiveway. Rather than focus on any one externality to the exclusion of other significant externalities, the Messiah proposedclubbing them together in to an aggregate measure of firm-level externality. Firms as diverse as power plants burning brown coal, armaments industry overstocking mines, missiles and grenades to sustain employment, mining, refining and shipping, and the pesticide industries preferring environment-damaging inorganic pesticides to safer organic alternatives, could pay off their residual, un-mitigated externality, whether associated with inputs, outputs, transportation, consumption or disposal, in the capital market.

The Messiah’s disciple wondered what theory, principles, or tenets underlay the claim to measure aggregate non-pecuniary externality, and how he would go about extracting it. Perhaps it was telepathy, perhaps the Messiah was in the mood to sermonize; regardless, he chose to reveal his logic. Short of claiming the Garden of Eden as his vision of Sustainability, the Messiah advised that no matter how wrong the world was in the present, it should turn sustainable at some future point in time. And if the roots of the current unsustainability could be traced to the industry, the seeds of sustainability too lay in reforming the industry. Since the equity markets typically operated with limited foresight, the burden of sustainability fell upon the bond market. It was by issuing long bonds to correct wrongs of the past that the Government turned the future sustainable (and financed its budget in the present). Greater the wrong, the more long bonds issued to fund remedial action across years, even decades (Fukushima?, Why does it ring a bell?). Thus, the quantumof, and price variations in the long term bond market gave an indication of the extent of the ‘externality’ outstanding. The Messiah simply ensured a balance between theexternality damages by the industry and the value of outstanding long bonds. It was by perturbing the balance while simulating a firm as a monopoly that he comprehensively gauged the magnitude of its externalities. These externalities were distributed among shares and traded away in a ‘paired-complement’ strategy by creating two externality-differentiated share and bond classes.

Despite his misgivings of correcting externalities by monetary means in an inequitable world (which pre-supposed, among other things, an efficient capital market, in particular a comprehensive Sustainability Index feeding in to Long Bond pricing formula), the Messiah went about his mission methodically. He firstcreated some terminology: an economy was comprised of ‘War Firms’ and ‘Peace Firms’. Firms that truly believed in sustainable production and manufacturing, regardless of how polluting or non-polluting their process was, were assigned the ‘Peace’ label. Hawkish firms that would rather generate excess, short-term profits than go the extra mile for sustainability were deemed ‘War’ firms. To denote the extent of potential gains in various market sections, he coined ‘ungodly’ phrases: ‘2key’, signifying large and immediate, if not ‘excess returns’ (the all too familiar ‘alpha’) as appropriate to the asset class, and ‘gas key’, denoting nominal returns, if at all. In between these extremes, he recognized ‘Bakey’ (residual), ‘Complements’ and ‘Shares’ (and an ‘Ookey’ was short for ‘You should know better’!). These constituted the various fractions of every pot of money no matter which asset class – whether equity, commodity, bond, gold, or realty. The 2key portion rewarded firms for meeting objective measures of achievement; the ‘Gas key’ was essentially a ‘Capital Protection Fund’ that provided funds to alleviate ‘performance deficiencies’in stock market firms if by merely adding volatility to those market sections. (It protected the sponsors’ capital while leveraging the short-term gains of speculators to cause volatility in the equity market). Consistent with the theme of his mission, the Messiah distinguished between ‘Externality Outstanding’, EO equity shares and ‘Externality Internalized’, EI shares.

In the next step, he conceptualized an ‘Externality Quotient’, EQ, acomprehensive externality measure representing the discounted inter-temporal monetary negative,non-pecuniary externalities as normalized by the outstanding equity base of the firm or industry. A pre-market session was designed to elicit the EQ, first for the benchmark ‘EI Equal Frontrunner’ firm (a technological and environmental leader), and then for other firms in the industry/sub-aggregate. After noting the initial ‘equilibrium’ equity and bond prices, the ‘Frontrunner Benchmark’, the Messiah ordered the simulation of each firm by projecting it as a monopoly firm operating at competitive aggregate industry price and output against a designated bundle of long-term bonds of value equal the aggregate equity base of the sector to which the firm belonged. The simulation induced a change in Sustainability indices to the extent the firm’s externalities differed from the Frontrunner Benchmark.The change in the price of the long bond bundle, post simulation, from its benchmark value due changes in the underlying environmental and sustainability indices of the long-bond pricing formula were noted. The projected Gross EQ of the monopoly was simply the change in the value of bonds relative to the ‘Frontrunner Firm’ benchmark. To obtain the net firm EQ, the Gross EQ was re-computed and re-denominated to reflect the firm’s capacity/equity share in the aggregate. That externality estimate was distributed across the utility’s base of equity shares as ‘Sustainability Deficit’, SD. Each SD-tagged equity share now represented a share in the assets and profit stream of the firm, as well as a share in the uncompensated, non-pecuniary externality liability it generated across space and time.

To ensure changes in price of long ‘SD’ bonds indeed measured an externality impact in the pre-open session, the Messiah insisted that a ‘Sustainability Index’, a Divisia index of underlying indicators, factor into LT Bond prices the impact of firm operation on EHS measures in the short, medium and long run. The indicators were chosen to represent various potential and significant damage classes. The sustainability indicators included factors as diverse as air, water and land pollution measures, as well as population, health and social indicators such as maternal and infant mortality, longevity, even violence and terrorism. These measures and indicators were themselves the outputs of underlying scientific, socio-economic and statistical models – measures that had real societal values attached to them but were not priced in to the products and equity shares. The Divisia module, equivalent to a reduced form of an externality costing model, indicated the change in long bond prices for various values of underlying determinants.

The SD-tagged ‘Externality-Outstanding’ (EO) equity share‘entitled’ the firm to generate a certain amount of externality in the course of its business. Every EO-EI share transaction in the equity market released an SD to the bond market where it was bid up or down and priced in to a longbond transaction, again of the same value as the equity transaction. Only upon the cancellation of the Equity SD-ticket in the bond market was an EO equity share converted to ‘Externality-Internalised’ EI share. The Messiah requiredevery ‘EO-EI-SD-ticket’ transaction in the ‘War Zone’ be matched by a ‘Sustainability Complement’ transaction involving a ‘Peace firm’. Thus, 2 SD-tickets were generated simultaneously from the equity market and transferred to the bond market for price-discovery and to sanctify the conversion of Long SD Bonds to SB status.

Anticipating the impracticability of every firm negotiating the bidding of its SD-ticket in the bond market, a recognized haven of the Greens, the Messiah willed a ‘Blue Optimism’ fund and ‘Green Caution fund’. The two funds took opposing positions in the Bond market and competed with other interests in the race to garner as many SD-tickets as possible. The winner - the side which converted all its outstanding SD bonds to SB and prematurely retired the bonds - qualified for a Closed-Cycle IPO 2key; the loser sponsored a ‘De-listing Bakey’. Between them, the bond funds brought about a slow replacement of ‘low dividend yield’ funds with new Closed-cycle ‘growth’ funds that enlivened the market with Growth 2key.

To hasten the transition to an ‘Externality-Internalized’ industry, the Messiah suggested a ‘virtual bifurcation’ of the stock market between the two share classes- EO and EI, the intent being to restrict certain funds and money pots to appropriate share classes.Lest there be a stampede overnight, only the ‘strictly 2key’ money pots – Growth, Opportunity, and Foresight 2keys - were restricted to the EI-section of the market, while the EO section was satisficed with Bakey, Shares, Complements and Gas keys. The Messiah’s ‘bifurcation’ induced promoters and shareholders to churn their shares from EO to EI earlier than they would otherwise, and brought about an early and comprehensive internalization of externalities. This churning of EO shares in to EI shares continued until the entire equity share base turned ‘EI’, and all bonds ‘SB’. At this point, the Messiah deemed the stock market to have ‘soft-landed’ and hailed the birth of an operating, albeit rudimentary, financially closed-cycle economy.

2key: Up to 95%; Share: 40-60%; Complement: 10-40%; Bakey: Residual, Gas key: 0-10% of ‘normal’ returns in asset class.

Now, the traders in the pit, the UPennFund managers on Wall Street,and Chicago Macro-economists pursuing their profession in the rarefied spaces of sky-high towers,alike,were in a tizzy as to how the system would adapt to the various stages of the macro-economic cycle. Once again, they approached the Messiah seeking his distilled essence. The Messiah obliged them, yet again. For each industry group, he used the pre-market session to obtain an estimate of the gross outstanding externality. He instructed the firms take sides – either ‘Peace’ or ‘War’ firms as appropriate to each. He then categorized investible funds in to ‘functional groups’: Growth, Risk Equity, Competition, Sustainable Development, Investment, Innovation, IPO, FPO– to name a few. Finally, lo and behold, the Messiah cranked up his ‘Mensa Economy'.

Boom time it was. Commodity prices spiralled up as the economy hummed and short-term interest rates firmed up. Equity prices, in particular those of ‘War’ and ‘Peace’ EO shares, gained traction. Shareholders in ‘War’ firms were beneficiaries of equity returns that were in consonance with the risk they had borne (Equity Risk 2Key). These firms also reaped rewards from a Commodity 2key Share - a return that supported Capital Retirement if in a Zero-sum with an Investment 2key in Long bonds.Peace firms, however, could only lay claim to a lesser return, a Growth 2key net of any inflation-induced bond impacts (a ‘paired fund’ return maximized by competition, hence Competition 2key). Both ‘War’ and ‘Peace’ firms shared in (own sector) IPO 2key in this phase of the economic cycle.

In the bond market, the Blue Optimism Fund exploited the low bond prices during the equity boom to buyback or exit SD-bonds while converting them to SB status by bidding away SD-tickets available at a discount from the equity market. The buyback enabled the Blue Optimism Fund to prematurely retire bonds, and facilitated the sponsoring of an IPO in the Equity market.

As the Economy peaked and entered the Bust cycle, shareholders in War firms enjoyed the Innovation 2key – a fund meant to support frontier, leading edge research. Both War and Peace firms enjoyed the Bakey returns of an Infrastructure investment fund whose primary gains went to LT Bonds. War firms were also favoured by an FII (Foresight) 2key, meant to pick winners for the early bird investor, andthe FPO 2key Satisfice, a strategic, thinly-disguised Monopoly fund, meant to expand market share by luring investors when most susceptible. These firms also benefited from a ‘paired Opportunity fund’ – a Stimulus 2key net of a Sustainability Bakey. Consistent with the Government’s view, the Opportunity fund ensured any gainaccruing to unsustainable War firms during the Bust period was ephemeral.

The story with ‘Peace Firms’ in Bust was quite different. Having accepted the vision of a sustainable industry, promoters and shareholders relied, on one hand,on the Infrastructure Bakey and a paired ‘Closed-cycle Transition 2key–TIPS’ fund, and on the other, on a paired ‘Balance2key’for equity gains. The Closed Cycle Transition ‘2key’ was essentially long bond returns net of inflation, a 2key maximized by a peaceful and cost-cutting, ‘Full Cost’ competitive economy. The Balance 2key, sourced from Equity Risk remnants (Gas key) and rising Long Bond returns, contributed to returns in this cycle, as did an Infrastructure Bakey camouflaged as Dividend 2key. In Bust, Long bonds attracted an Infrastructure 2key, a Sustainability 2key supported by excess Gold returns (Gold 2key), an Arbitrage 2key from equity and currency markets, and nominally, some Closed Cycle funds to enable aspiring firms to weather the ‘winter’. The Capital Protection Fund, CPF, (a Gold Gas key and a Commodity Gas key) preserved gains from Gold and Commodity markets among Peace firms while sowing the seed for a future 2key return. The Green Caution Fund exercised its option to bid up SD-tickets with the proceeds of its redemption from Long bonds from Peace firms even while investing in them on the equity side of the market.

In the ‘Hard Assets’ category – Land and Realty, the Messiahtrudged the simpler path.A Realty 2key supported Land prices during Bust period, while a Land Bank 2key and a Gold 2key Complement underwrote gains in Realty prices during Boom. A Land Bank gas key supported land assets in Boom, and realty assets in Bust. A Gold gas key added to Volatility in the Realty assets during Bust.

And as far as Currency markets were concerned, the Boom period was characterized by 2keys from Exports, Foreign Exchange Hedge, and FII Hedge pots. In the Bust cycle, currency markets moved with an Import 2key, and Foreign Exchange Hedge key, supplemented by FII gas key and Export gas key. A TIPS fund was distributed in 2key and gas key between the Boom and Bust cycles, albeit with a sting in the tail.

Having discussed threadbare the ideal operation of the stock market, the Messiah, sought to reinforce its utility by mentally simulating a policy goal to eliminate or minimize the Armament industry.He firmly believed that an industry as ‘bad’ and one as close to the government and its secrets as the Armament industry, would survive and proliferate, even if it meant the destruction of nations and their economies. The Messiah’s dilemma was how he would put an end to the scourge that robbed the global citizen of bread on his plate and returns in the market? How would he wind up an industry that had a long record of engendering technical innovations that bolstered the productivity and efficiency of industrially advanced nations, created business opportunities and sustained jobs – the very measures by which the Government and politicians were judged by the electorate? Could he not just give the industry the Christmas week and bull-doze the factories for bread lines come January 1? If the Messiah was no simpleton with child-like innocence camouflaging ignorance, thanks were in order to the Big Lord!

But seriously, the Messiah was aware, that behind the various wars and factional strife, was a coterie of advanced nations and industry barons heavily invested in mining and basic metal firms, in technology supporting those industries, as well as in commodity markets transacting the outputs of those industries. Fact of matter, the Messiah was so wise that he had a downright ‘unholy’suspicion: Could it be that the stakeholders and investors in those industries were forced to resort even to war to recover their investments that had been eroded by the umpteen stock market speculator-day traders? Perhaps Governments that had promised a 100% ‘Total return’ in the capital market to Hard Rock Mining and Basic Metal Industry, HRMBM firms, were obliged to consider novel ways - war and ‘peace-missions’ - to keep them, even if it meant the world was a last few steps away from a WW-III Armageddon?

Fearing the worst, the Messiah came up with a two-pronged ‘Carrot and Stick’ strategy. He decided he would, on one hand, offer the HRMBM industry a reasonable return for the risks they endured by sponsoring a ‘Stimulus 2key’ that stimulated economic demand and raised the standard of living of his followers, and on the other, simultaneously offer the armament industry an incentive to ‘downsize’, an opportunity to innovate in to a ‘non-military’ firm, and an opportunity to generate a ‘peace’ return on its investment while refraining from weapon production. To keep incentives straight, the Messiah exploited differences in intentions and outcomes between the two industries to promote a third party, Agriculture.

To facilitate the realization of the policy goal, the Messiah paired the Armament industry with the HRMBM industry, pitted them against ‘Peace Hawks’ (International Organizations) and Agriculture interests in the Bond market, and initiated equity trading in a ‘bifurcated’ stock market. In the boom-time economy, a Promoter of the Armament ‘War’ firm holding EO shares sought 2keys to realize capital gains, but was denied the same from lack of EI status. Unable to realize capital appreciation, his options were either to lobby and induce foreign policy mis-steps that enabled him to secure armament orders and exploit the Armament 2key, or fold in and submit his shares to the EO-EI conversion program. Sanity and good-will prevailed, and the Armament industry weighed its Externality Quotient in the pre-market session with intention to convert all EO shares to EI status, if eventually. As if walking a balance beam, the promoter sought to optimize, on one hand, the harvesting of 2key returns by releasing as many EO shares to the market as possible without compromising on share price, and on the other, minimize the loss of capital appreciation in the EI side of the Equity market from a delay in offering EO shares to the market. Avoiding the Armament 2key trap, he sold his EO shares to realize a ‘Depreciation2key’ with which to retire Armament production lines. The Buyer was an International Organization that monitored International military relations and managed a Peace Dividend fund. The transaction triggered an ‘SD Complement’ in the ‘Peace zone’ and an SD-ticket in the Bond market. An HRMBM ‘Peace’ firm pounced on the SD Complement and executed a similar trade to realize a ‘Competition 2key’.

Following the equity market transactions, the Bond market announced 2 SD tickets – one each from the Armament firm and the other from the HRMBM firm (both with a floor price supported by the UN/GEF/WWF). The SDs were bid up to different extents by bond market participants. The Armament SD, prized for the large risk to international peace that the industry had caused, was, again, bid away by the Peace Hawk whoapplied ‘Peace Dividend’ funds to buy in to the Bond market (which rose with infusion of the Peace Dividend 2key Share), thus ensuring a presence on both sides of the market. The HRMBM SD, comprised largely of damages to soil and ground water, was of particular interest to NABARD whose mission it was to support agriculture and which had issued agricultural bonds. It bid up the ‘exernality sin’ manifest in the SD tickets and won the right to retire the bonds prematurely when it had ‘redeemed’ sufficient number of SD tickets representing EO shares of value equal outstanding bonds in the market. The NABARD used the proceeds of the prematurely retired bonds to buy in to Land for agricultural use, thus offering a Land 2key to those invested in the asset.

In the Bust cycle, the Armament War firm had many takers for its EO shares. Shareholders had a choice between a Stimulus 2key, Innovation Funds, and Opportunity funds when offloading shares in the market. The Stimulus 2key supported Armament firms to the extent their output served non-military purposes. The Innovation 2key supported strategic research, albeit not necessarily peaceful or ‘Closed cycle’. Thus, the International Organization found it to its advantage to support the Armament firm with an Innovation 2key, and, simultaneously, buy out the SD ticket to consolidate in or exit the Bond Market. The Messiah also offered an Armament 2key, itself a Zero Sum with the Peace Dividend 2key, but only in Bakey, and only to holders of the Armament firm’s EI shares. The strategy restricted capital appreciation and ‘alpha’ to those Armament firms that had substantially converted their share base over to EI status and those that abjured the War route to profits.

The unconverted HRMBM Peace Firm EO shares, besides attracting Stimulus funds, found buyers in Closed Cycle proponents and Balance funds – the former seeking profits from lower cost consequent to enhancing the efficiency of material balances in the firm’s production process, and the latter seeking to profit from correcting the inefficient use of mining and refining capacity for production and stockpiling of arms.

In subsequent cycles, a dominant shareholder in the Armament industry, perhaps a Promoter, secured both the Armament 2key bakey for refraining from Armament production and stockpiling, and a Capital Depreciation/Retirement 2key for his ‘War EO’ shares (The Depreciation 2key was a Zero-Sum with an Investment 2key, both of which were sourced from returns generated in the Commodity market). The Capital Depreciation/Retirement2key was secured from a Peace Dividend Bond foreclosed by bidding away Armament SD-tickets in the bond market (which enabled the Promoter to claim EI status for his shares, a pre-requisite to de-commission an Armament production line or factory). The de-commissioning of Armament factory and/or the reduction in armament stockpile reduced the risk of war, which was an important factor in determining long bond prices. The consequent increase in bond prices was a reward to the Institution sponsoring the Peace Dividend Fund. The churning of the Armament EO to EI shares, induced a similar churn in the HRMBM shares, purchasing the SD-tickets from which enabled NABARD to retire its Agriculture bonds and channel them to purchase land for agricultural use – perhaps a harbinger of a nascent green revolution.

Armament factories outta business, sustained profits for metal and mining industry, a resurgent agriculture sector, an environmentally sustainable industry, and a financially-closed capital market? One would be excused for congratulating the Messiah for showing the path to sustainability, if not salvation. But the Messiah cared not to learn if his followers were ingrates. For, as he trudged his lonely path to the setting sun, he was wise to the nefarious, grand designs of those un-named bent on exploiting the opportunities and loopholes in his proposal and get the better of God in his own paradise (even if it meant a parallel, underground stock market and 8-figure signing bonuses for fresh Ivy League graduates !)

Subscribe to:

Comments (Atom)